(category)Mutual Funds

How the Mutual Fund Total Expense Ratio (TER) worksHow the Mutual Fund Total Expense Ratio (TER) works

A deep dive into the nuances of mutual fund expense ratios. We discuss the hidden costs of owning a mutual fund, explore various trends, and how costs can affect your investment outcomes.

Deepak Shenoy•

We do not attempt to answer such deep questions.

But yes, it's called the TER, so we'll just dive into it futher. The TER is a part of the cost of investing in a mutual fund. Mutual funds are run by "Asset Management Companies" (AMCs) and there's fees, costs, taxes and a bunch of things that hit the fund's cost structure beyond the prices of the shares and bonds they buy. That "extra" is what the TER is supposed to be.

(Oh, and it isn't "total", because the TER doesn't include some costs, which is like "100% vegetarian but could contain egg", we know)

What we'll go through:

- The Expense Ratio doesn't matter as much as you think

- The TER isn't everything: What it is, what it doesn't include, and the limits that funds can charge

- Understanding the regular and direct TER for funds

- They can change the TER! And yes, they do, more often than you think

- The Passives and the Liquids: where TERs probably matter the most

- A SEBI proposal to change the rules for TER

- That's all.

The TER doesn't matter as much as you think

The expense ratio is, for the most part, what you pay to be able to buy and own a fund. Note that it is different from an exit load, when you pay a certain amount to sell a fund within a certain period of time, and that load goes entirely to the fund itself, benefiting the remaining unitholders (not the AMC). An exit load actually helps the fund. An expense ratio or TER takes away from it.

In India, mutual funds have to report their NAV after deducting all expenses, so your definition of returns itself are after-cost. You might then wonder whether you should care about costs at all.

Or put simply, if a fund is giving you good returns after all costs, should the expense ratio even matter?

The correct answer is: no, it doesn't matter. If the returns are index-beating, or meeting what you expected, then it's irrelevant. Because when you sell, you'll make exactly what is in your NAV. (And because we finance people are complicated, we have to add: minus stamp duty, exit load, STT or capital gains taxes, but if we go into that you will be reading this into 2025)

So, it doesn't matter only where your fund management is giving you super-returns. In some cases, where all funds are roughly the same, then it will matter - because that's the only way to differentiate them. Let's go through the motions.

Remember this:

- A mutual fund is structured as a trust

- When you buy units as an investor, you pay into the fund's bank account, and the fund issues you units

- The fund buys stocks and all that

- 1. the fund pays brokerage and audit costs

- 2. the fund also pays commissions and marketing expenses

- 3. the fund then pays the Asset Management Company (AMC)

- The 1+2+3 is the real expense ratio, but you get a subset of it displayed to you as the "TER".

What you see isn't what you get, though. While TER covers most expenses, it does not include everything. What isn't included?

- Brokerage and transaction costs upto 0.12% of the AUM for stocks, and 0.05% for derivatives are not covered in the TER

- STT (Securities Transaction Tax) which is included in the buy or sell price and thus, "capitalized" (you don't see it as a cost at all). This is 0.1% of each buy or sell transaction.

- So, if an equity fund turns over 50% of its assets, theoretically that's an extra 0.22% that you might not see. Considering that expense ratios for equity funds are usually between 0.5% and 2%, this is a significant cost that could fly under the radar.

- GST (this is currently outside the TER limits)

- 0.3% for funds from outside the top 30 cities

- 0.05% more for funds that charge an exit load (this is voluntary but most charge it)

As you can see, it's anything but "Total Expense Ratio".

The Regular and Direct TER for mutual funds

When you are ready to invest in a fund, you have two options:

- the regular plan: a distributor like a bank or an individual helps you invest, and they make a commission that's part of your "regular" TER.

- the direct plan, where you invest without any intermediary, directly. Here the TER is lesser.

Both plans have the same portfolio, and are managed by the same fund managers. Where they differ is in their expense ratios and NAVs.

In short: Regular TER = Direct TER + commissions.

Since direct plans don't involve any third-party, you save some cost, which gets added to your returns. In regular plans you pay the distributor a commission so your returns are lower to that extent. These costs matter, and can affect your fund's performance versus the market. This table shows how active funds have fared in the past few years, from a SEBI paper:

Clearly,

- As highlighted in green, direct plans show a far more consistent track record of outperforming their benchmarks compared to regular funds.

- The reverse is also true. Regular plans have a higher tendency to underperform their benchmarks as shown in red.

(You might see that only 44.77% of direct plans beat their benchmark - that's actually misleading because many funds have very tiny AUM and they get counted alongside the larger ones. So the argument here is only that Direct does substantially better than Regular)

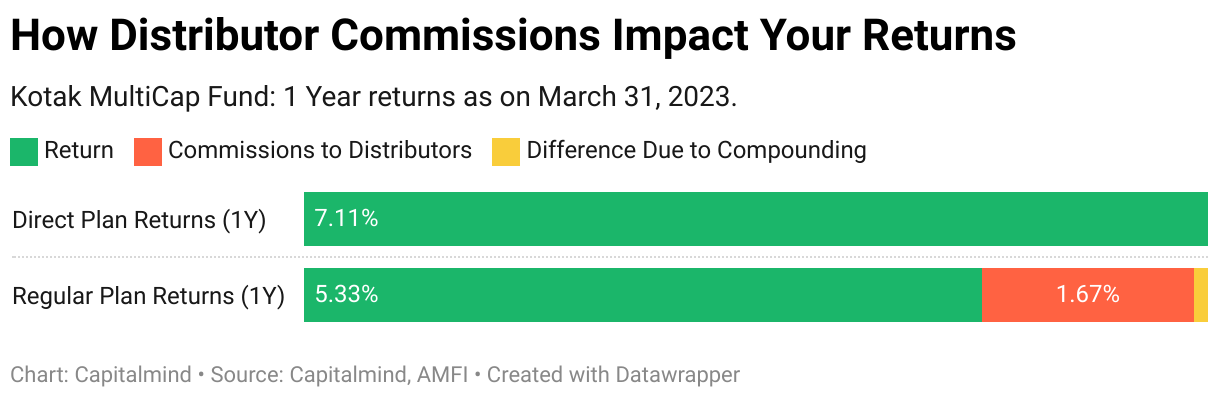

Take Kotak MultiCap Fund as an example. If you invested in the fund's regular plan on March 31, 2022, your returns would be lower by 1.78%, due to the commission being paid out to your distributor:

This fund is just an example, but the story is the same for all funds.

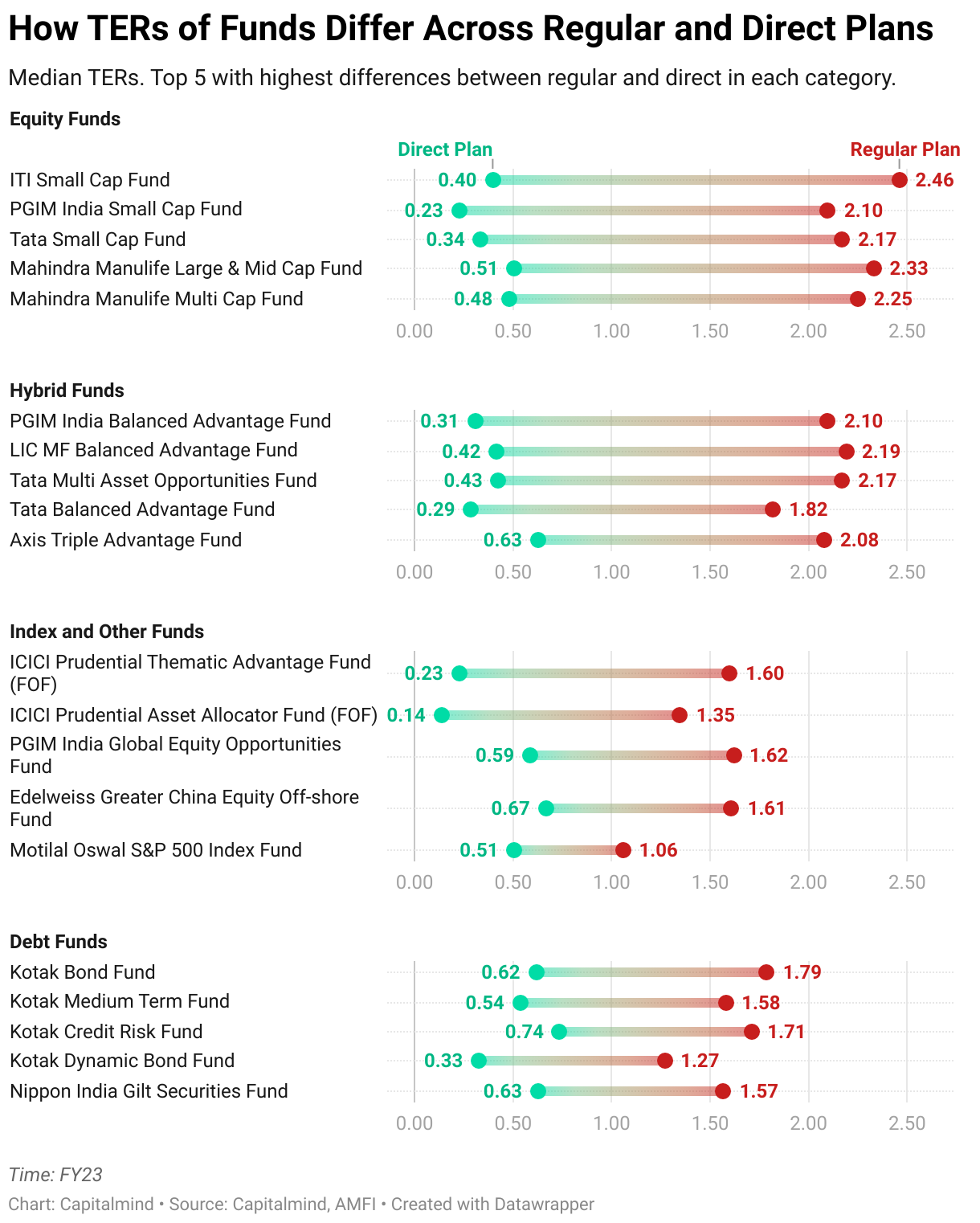

The table below shows funds from each asset class with the largest differences in costs between regular and direct plans:

Smaller funds with lower assets under management (AUM) seem to have higher differences in expense ratios between regular and direct plans. Meaning: they pay higher commissions to distributors, simply because they're small and want to grow..

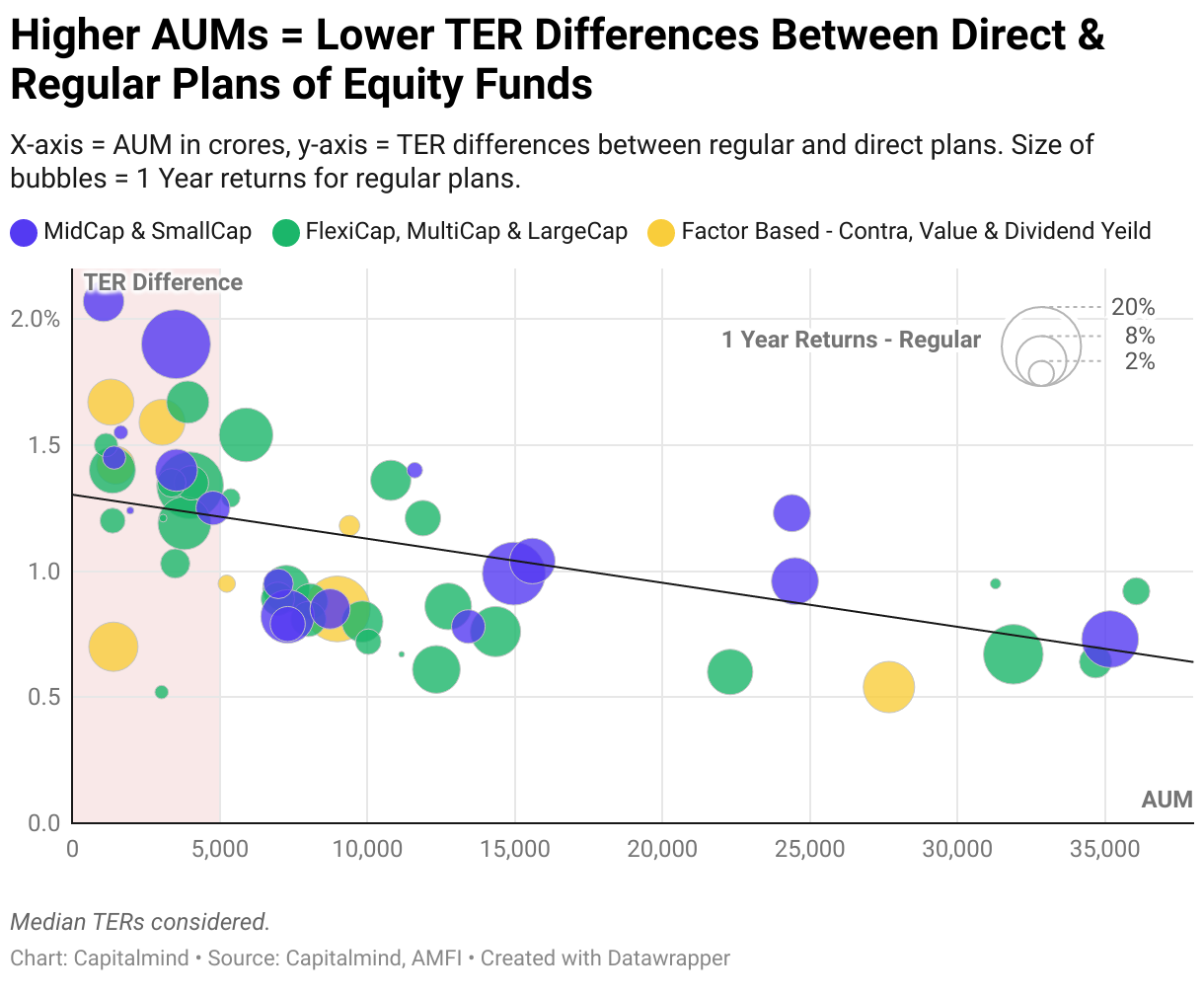

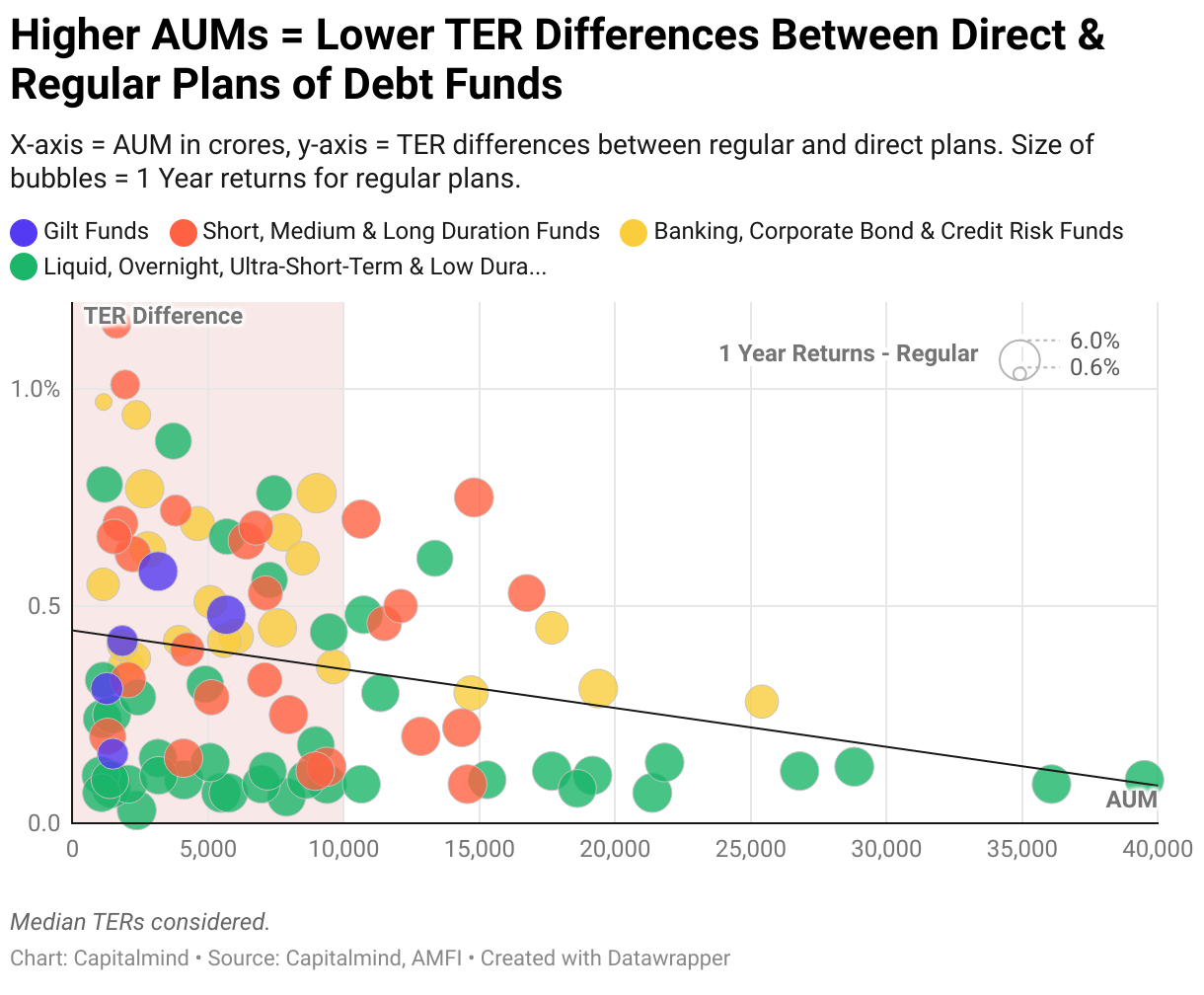

Is there a correlation between size (AUM) and the commissions paid? Here's a graph that shows it:

The X-axis shows AUM of the funds in crores, while the Y-axis shows the difference in expense ratios between Regular and Direct. The bubble sizes represent the funds' one-year returns of regular plans.

We see that:

- Funds with less than 5,000 crores AUM, highlighted by the red-shaded region, charge roughly 1% higher for regular plans. Larger funds have lower effective commissions.

- Bubble sizes don't particularly show a trend, meaning that while certain funds pay higher commissions, they're not able to get a much higher return just yet. (You'd pay higher commissions to get higher returns)

Debt funds show a similar picture, with smaller funds (< 10,000 crores) showing higher differences in expense ratios between the two plans. And since these are debt funds, returns don't vary a lot anyway, so again higher fees for the fund are not usually justifiable by returns.

Expense Ratios Can Change Anytime

Now, we run a Portfolio Management Service at Capitalmind, so we're biased. But in a PMS, expense ratios are pre-determined: if you're paying 1%, that's what you'll keep paying. This cannot change for the duration of the PMS agreement.

But with mutual funds, it's a different story. They can raise (or lower) their expense ratios anytime. So, you might have a fund which has given decent returns, but if it suddenly hikes its TER one day, your returns will feel the pinch going forward.

This didn't sit right with SEBI, so they stepped in and:

- made it mandatory for fund houses to give you a heads-up every time they change their expense ratios, and

- asked mutual funds to reveal daily TERs on their and AMFI's website for transparency.

But, the rules didn't stop many funds from regularly changing your TER anyhow. Here's a table which shows direct equity funds with the biggest jumps in expense ratios last year. Investments in such funds at the start of the year would see costs surging 2-3x in many cases.

Many debt funds, which generally have stable costs as they're mostly owned by institutions, also hiked TERs by over 10 basis points, or 0.1%.

The takeaway here is, monitor the expense ratios of your funds now and then (available at AMFI's website here), and avoid funds with unjustifiable increases in cost.

Liquid and Passive funds: execution matters in passive

Here's the thing with passive and liquid funds – they are all pretty much the same.

In liquid funds, managers can't make as big a difference in returns by picking different securities, as they can in other fund categories. In passive funds, managers can't make active calls at all – in fact, there's a maximum tracking difference allowed.

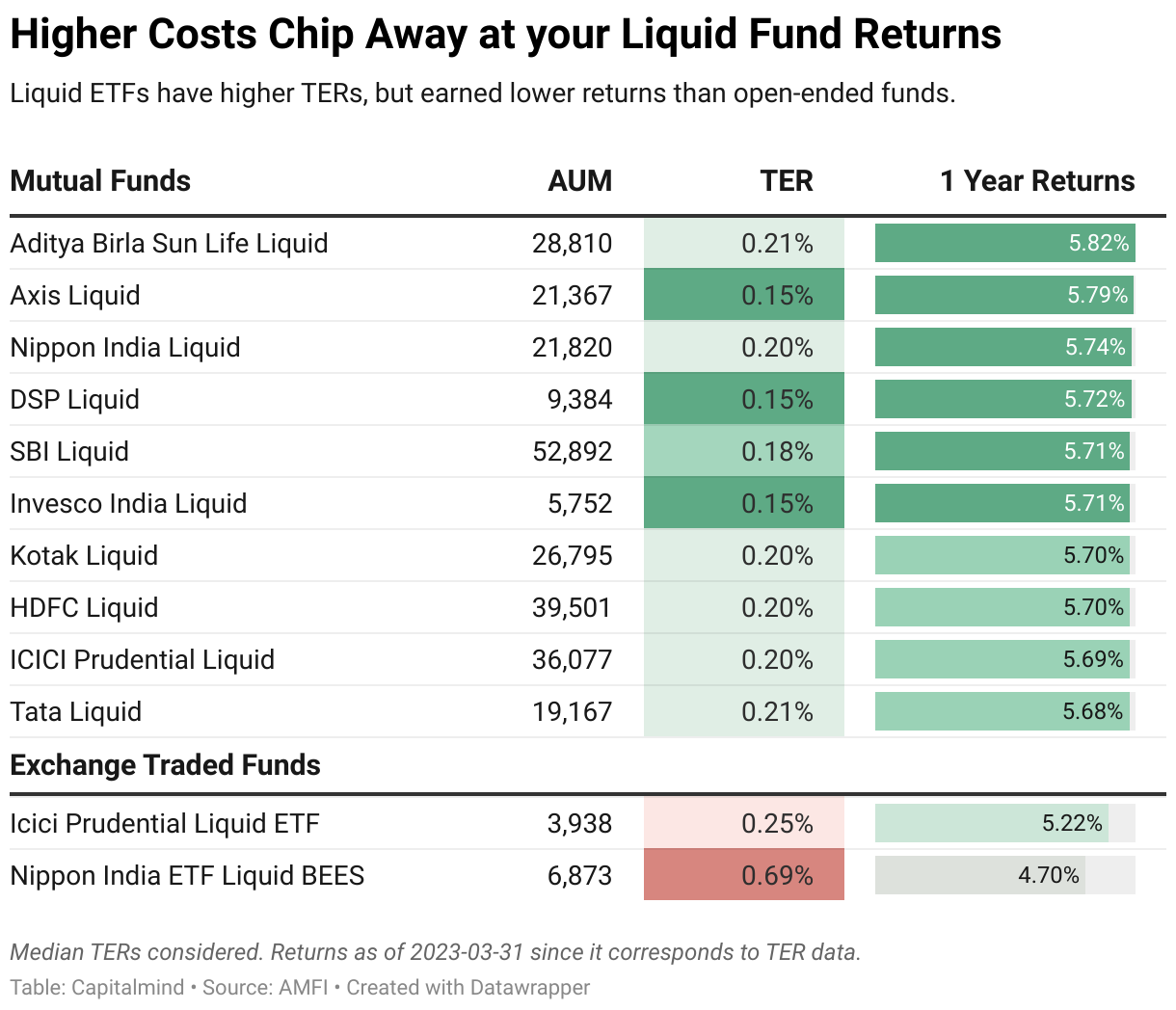

If returns are similar, why should you pay more for one fund compared to another? For liquid funds expense ratios matter the most. And since returns are more or less the same, higher cost = lower returns. The table below shows expense ratios and returns of liquid funds in FY23:

Last year, liquid ETFs charged higher expense ratios than liquid mutual funds, leading to lower returns.

Also, worth noting, Nippon's Liquidbees charges (now) 0.69%. That's huge, you'd think. But it has become the 'Maggi' of liquid ETFs – it has become the name that people associate with the category. Because of this “brand”, it has a higher AUM at lower returns, and can charge a higher TER even though it doesn't really offer anything special.

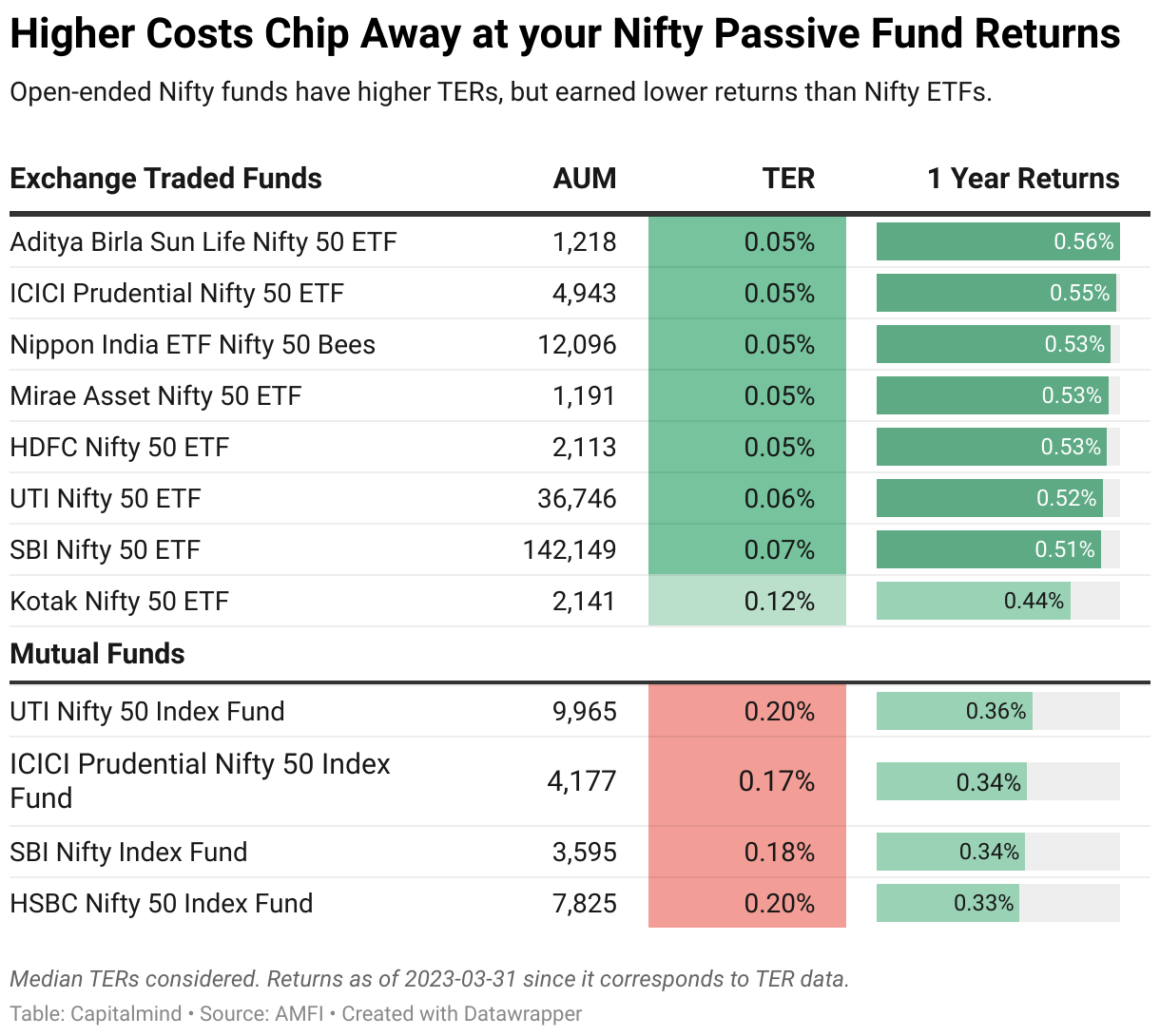

With index funds, it may seem like a similar story, but in reverse. Nifty mutual funds had higher expense ratios, and they reported lower returns than Nifty ETFs in FY23:

ETFs don't incur STT like mutual funds do. They are incurred by market makers, who then sell at a premium in the market. So in this case, Nifty ETFs make higher returns simply because the STT cost isn't there for you.

Make the comparison within mutual funds, or ETFs, not across categories. Our video explains:

Read about how index funds and ETFs behave and how to choose them.

With index funds (not ETFs) there is something strange:

- UTI Nifty Index fund (our choice in the video) outperforms even though it has a higher expense ratio (0.20%) versus others (0.17% or so).

- That's because they do better execution and take advantage of size.

So over at an Index fund, costs don't matter. What you care about is: what's the real expense ratio? Compare all funds tracking the same index with their tracking difference i.e. return compared to the benchmark, and choose the one that's consistently better than the rest.

TERs aren't infinite: SEBI has limits!

On the flip side, SEBI says hello, if you manage too much money we're going to cap the maximum TER you can charge. Beyond a certain scale, costs don't go up with AUM, so companies should reduce their fees, in SEBI's terms.

Currently, the tiered structure applies on a scheme level.

Note that specific exclusions (non-top-30 city aum based expenses , exit load based expenses, brokerage, STT and GST) are not part of the above limits.

Let's take Parag Parikh's Flexi Cap fund as an example. As of writing this, the fund has 33,600 crores in assets.

Consider this: Parag Parikh Flexicap fund, even after gathering 33,600 cr. (one of the largest active equity funds in the country) still charges close to the limit at 1.37% TER (Regular plan) plus then additional 0.05% and 0.09% under other parts, taking expenses to 1.51%.

But, SEBI has, in a consultation paper, questioned this. (link) The current limits consider AUM at a scheme level, and SEBI's saying the spirit of the limits (i.e. that AMCs have scale and should be way below limits) isn't being honoured.

They're saying:

- Benefits come at an asset class level. For example, a team managing a debt fund is likely capable of managing another similar fund.

- The current structure encourages the industry to redirect investors from large schemes to smaller, or even newer ones, which attract higher TER.

- So instead of a single fund having TER limits, they want to limit the TER of an entire AMC (separately on equity and non-equity, but not at a single scheme, but across all schemes together)

- Strangely, this calculation for hybrid funds would be on a weighted average basis—perhaps discouraging managers to taking debt calls.

SEBI estimates that if its new proposals had been applied during FY22, the total expenses charged to investors would have been 4.55% lower at the industry level.

Will SEBI change the TER game?

SEBI has a new consultation paper on TER and this might change the game:

- TER should include all costs including transaction related costs such as brokerage, GST, STT, etc.

- So you churn more, and you might hit TER limits sooner

- AMCs might directly trade on the exchange, reducing brokerage costs even more

- Get rid of the non-top-30 city expense ratios and the exit load extra fees.

We'll have a podcast on this soon.

Wait, what extra charges do they have?

Funds can charge an extra 0.3% if they're attracting substantial business from smaller cities (named Beyond Top-30, or B30). These extra charges are meant to encourage distributors to bring in investors from these cities.

The specifics are:

- at least 30% of the gross new inflows in the scheme

- or 15% of average assets under management (year to date)

- whichever is higher.

What this means for you is, if your fund is making inroads into smaller cities, it might be nudging up your costs. Often these investments are shuffled around by distributors, after the minimum one-year period ends. They advise clients to withdraw their money and invest it in other funds to get the B30 commissions elsewhere.

SEBI looked at this and said no way. They also noticed some fund houses applying B-30 charges selectively, and not in others where it benefits them to keep TERs low. So, in the new paper:

- Do a PAN check so the same investor doesn't requalify to pay higher fees to the AMC

- Cap such commissions at 2,000 rupees.

- Clawbacks of the higher fees to ensure there is lesser churn

Will the new rules change things for AMCs?

We'll do a post on the economics of asset management companies, where beyond a point, it's substantially higher return on incremental AUM because costs are relatively fixed. The new rules will hurt the AMCs somewhat, by capping what they can charge when they grow, but in a highly competitive environment, that should have been the case anyhow. However it will hurt their economics quite a bit in terms of percentage (They might see lower profits by 10% to 30% depending on mix)

Secondly, the problem isn't really that AMCs are charging 0.15% more than they should - for a large number of funds, the new rules will only benefit investors by that much. The problem lies in unlimited distributor commissions within the TER, where an economy of scale still results in lower costs, but SEBI doesn't want to limit what distributors who have scale (like banks) can make.

For investors, the problem simply is: Total Expense Ratio is not "Total" at all. If SEBI fixes that, we should have better comparisons of cost and return going forward.

Wrapping up

Understanding expense ratios is critical for smart investment decisions. The key points to remember are,

- Opt for direct plans if you understand how to select funds. Commissions to distributors are justified when they provide solid value in helping you select and stick with funds longer term. Bankers generally change too often to provide value, so you might want to avoid using them (the bank will get commissions forever) but other organizations may do better.

- TERs can change daily. Monitor your funds expense ratios.

- While choosing which funds to invest in, keep an eye on costs holistically. Some costs can fall outside of TER

- TER is not useful when analysing active funds; their returns are net of costs, so there costs don't really matter.

- In liquid funds (and most debt funds) higher costs will generally hurt performance more.

- In index equity funds, check the performance drag (tracking difference) with the index and choose a fund with more consistent performance closer to the index.

- SEBI's new proposals can substantially change the game.

In the end, returns are the only thing that matters, to most people. Costs don't matter if you compare on returns alone, but sometimes, it's useful to know that your costs could be changing, and that will impact how your returns will be in the future. Pay more for a higher return - that's a nice thing. Pay more for good advice, that's also useful. But know what you're paying for.

Related Posts

Make your money work as hard as you do.

Talk to a Capitalmind Client AdvisorInvesting is not one size fits all

Learn more about our distinct investment strategies and how they fit into your portfolio.

Learn more about our portfoliosUnlock your wealth potential

Start your journey today