You’re not going to believe this, but these Index funds are awesome, I say. Capitalmind’s Passive portfolio – a smart combination of Index funds – is now among the best performers of all large cap mutual funds, any time in the last three years.

With a simple combination of India’s top 100, and from last March, the US Tech top 100, the returns seem seriously good; and think about it: There’s no analyzing stocks, there’s no need to “change” the portfolio because oh banks are going to fall or oh, maybe that stock is better and so on. Whatever gets out of the top 100 is out, automatically, and the new entrants are in. Automatically.

And our combination has the Indian biggies of HDFC Bank, TCS, Reliance and so on. But also the US Tech biggies of Apple, Microsoft, Facebook and even Tesla now!

We decided to compare this combination with all the larger cap funds – some of which are now flexi-cap funds. The result is that if you look at the CM Passive portfolio it simply beats most of the large cap funds at most times. Since 2018, when rules for large cap funds forced them to invest most of their money with large caps only, the outperformance of our index portfolio backtest is stark.

CM Portfolio uses a Nifty ETF, a Next 50 ETF and a Nasdaq 100 ETF returns. We rebalance to 1/3rd each, at the end of every year in the back test.

Note: we have included an additional 0.25% per year “fee” for the CM passive portfolio. This is to include the cost of slippage or perhaps a fee you might pay a manager like Capitalmind Wealth.

If you can’t see the above, here’s an image:

Note that since we started from 2013, we had to take “regular” funds. But direct funds – which started in 2013, would do better by about 1% to 2% a year. If the performance was that close, I’d say it wasn’t useful at all. But no, the answer is clear: the underperformance is much much larger.

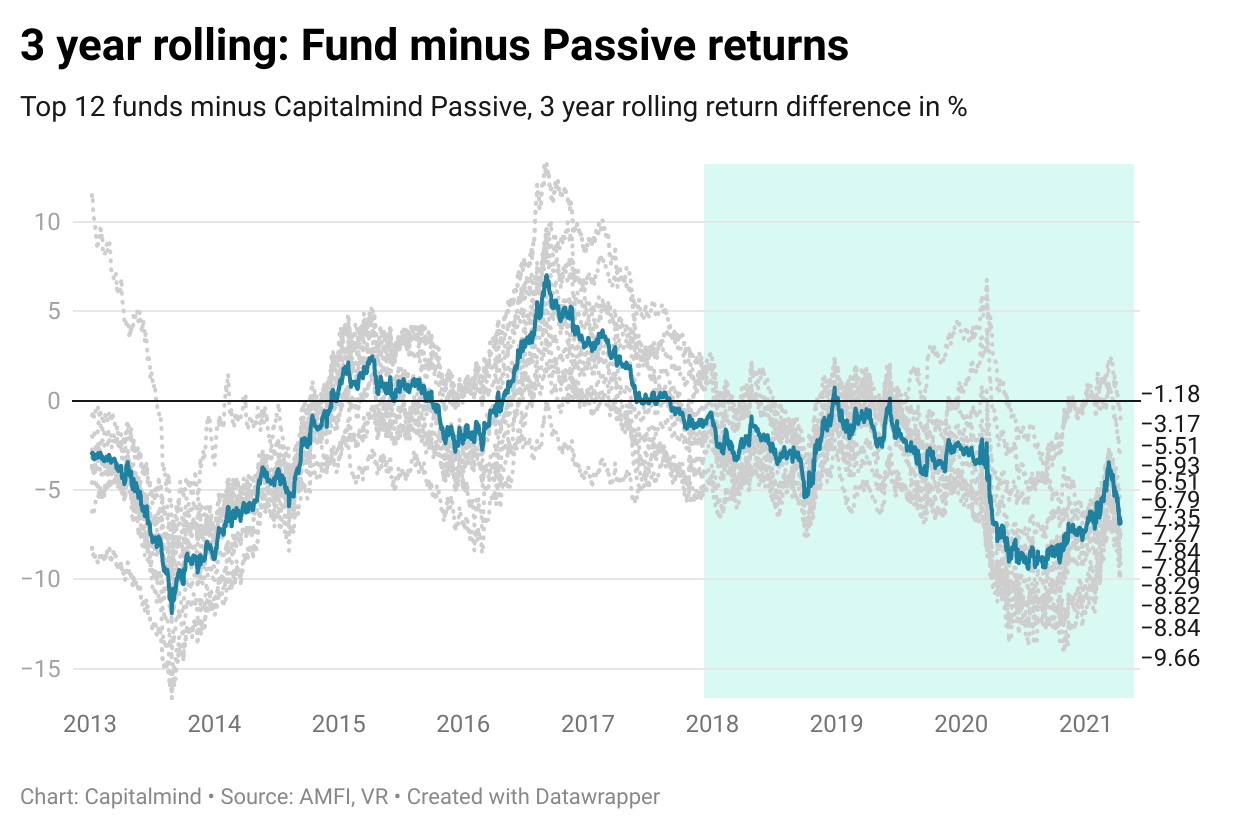

Capitalmind Passive beats Large Cap Mutual Funds Most of the Time

This is evident from the graph, at least from 2018.

Take a deeper look: If I take three year returns at any point, of each fund, and minus from it the CM Passive returns, you can then see which funds beat the CM Passive Strategy. Most, however, have simply not done so, and we see the underperformance (that is when the grey lines below go under zero) increasing since 2018.

The dark line is the average of 12 large cap mutual fund returns, three years rolling.

The dark line is the average of 12 large cap mutual fund returns, three years rolling.

As you can see here, the average underperformance is close to 7% per year! Even the best fund at the moment – UTI Equity – underperfomed on a three year rolling basis, at -1.2%. If you take UTI Equity’s DIRECT plan, it would have still been lower by 0.2%.

Note: The CM Passive fund back test subtracts a 0.25% cost of management/slippage etc.

Why do large cap funds underperform?

Three major reasons, we think:

- Fees: the fee drag on large cap portfolios will hurt. Whatever you do, you need to outperform by at least 1% to make up for fees.

- No edge: Everyone’s chasing large caps. There’s no edge that anyone has. Plus, new rules like recently, where SEBI said you have to even make private meeting recordings publicly available for listening, will reduce this edge even more. If you don’t have an edge, how do you outperform?

- SEBI’s restrictions: These allow large cap funds to focus among the large caps only – 80% of their portfolio has to be in the top 100 stocks. So you can only change the quantity of some stocks versus others, you can’t really buy into smaller stocks to spruce up returns.

The other elephant in the room is that EPFO, India’s provident fund giant, is mandated to invest 15% of flows into equities, through Nifty and Sensex ETFs. That means the indexes and the stocks within keep getting these inflows, in the weights of the index. SBI’s Nifty ETF is the largest fund in the country at 95,000 cr. – mostly due to EPFO inflows.

(The largest active fund is Kotak Flexicap, earlier known as Kotak Standard Multicap, which is at 34,000 cr. and about 65% lower in assets than the SBI Nifty ETF)

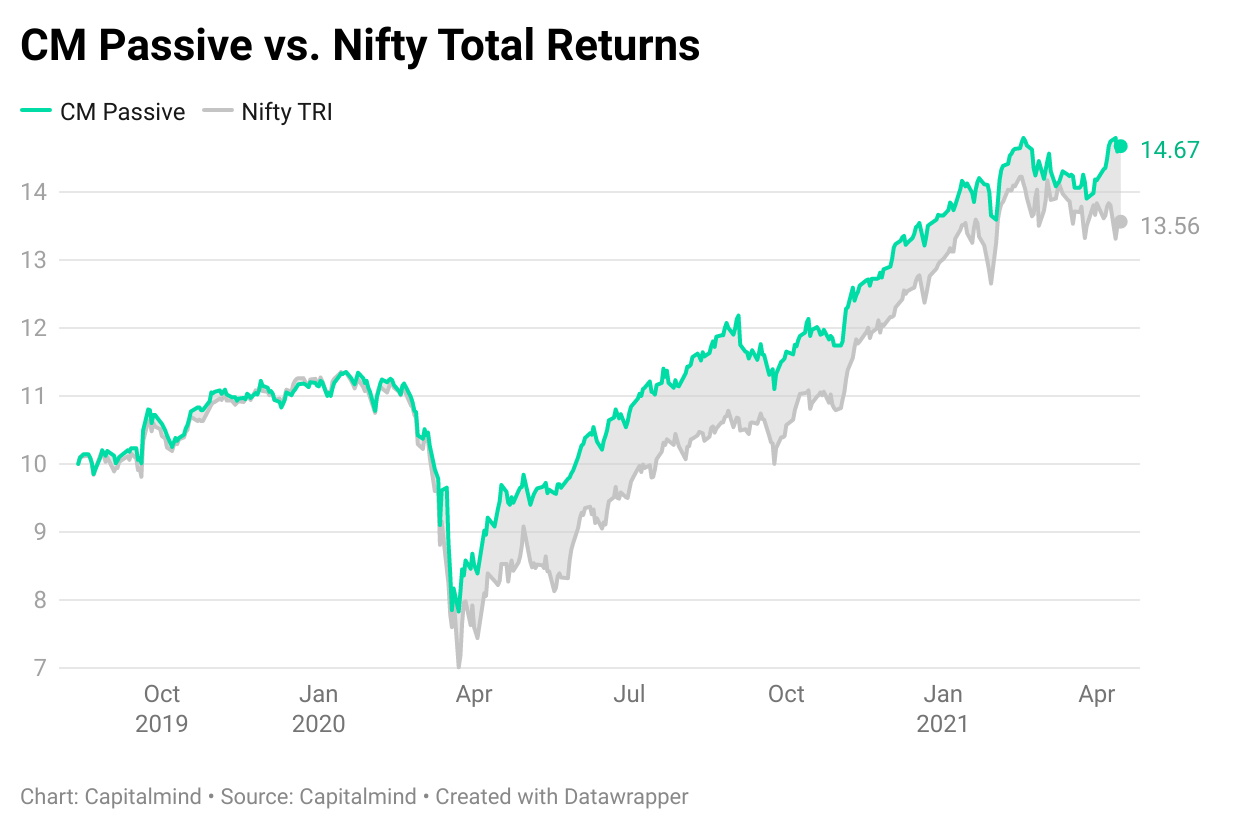

Actual underlying performance using ETFs

We track our actual performance using the ETFs we have used. CM Passive has returned 46.7% from Inception, whereas the Nifty itself is only 35.6%. This outperformance is largely due to the US Nasdaq 100 that we added in March 2020.

The change: EPFO’s Accounting forces our hand

Out of the blue, the SBI Nifty ETF gave three dividends last year, adding up to about 4% or so. This sucks because dividends are taxed now.

Why did they do it? A complex accounting reason:

- EPFO invests in the SBI Nifty ETF

- EPFO must invest 15% of flows into the equity funds

- EPFO also decided to give a huge 8%+ return for the last year.

- How can it, when even government bonds, which are the largest chunk of EPFO holdings, are only giving about 7%?

- The answer: sell some of the equity funds bought earlier – the SBI ETF was one

- But if you buy 15% and sell 5%, the net purchase is only 10% (of whatever money EPFO gets every year).

- Which violates EPFO’s requirement of minimum 15% of net inflows.

- So EPFO went to SBI and said, please give us dividends instead.

- And SBI complied, thulping the rest of us with a taxable dividend. (EPFO pays no taxes)

This is likely to continue next year as well. So we will take action.

Our action is:

- For all new purchases, we move to NIFTYBEES and JUNIORBEES in the Capitalmind Passive Portfolio (ETFs)

- You might end up with huge taxes if you sell the SBI ETFs now.

- So leave them as is and don’t sell.

- If the market were to crash, you can sell and replace with the BEES ETFs as mentioned above, which lowers your tax bill. Till then, just hold.

- We recommend rebalancing back to 33% for each position, at the end of a year.

Note: if you use the CM Passive portfolio through mutual funds and not ETFs, you don’t have to change anything. The funds don’t pay dividends.

More reads:

- We start the Index based Large Cap Portfolio (August 2019 – Read post)

- The Passive portfolio structure

- The full passive portfolio for subscribers.

- Factsheets: (Feb 2021, Jan 2021, and more)

Aside: Why do we recommend Passive Funds?

They’re doing well. Really really well. And we offer them at our PMS too, at Capitalmind Wealth. In real terms, post fees, this simple index portfolio seems to have been at the top end of performance over the last two years – even after you include brokerage costs, Capitalmind fees, STT and GST. (Only Momentum has done better, and Momentum is our flagship model portfolio both at the PMS and for Capitalmind Premium)

Please also read the Capitalmind Wealth PMS Index Portfolio White Paper.

We believe that for the performance, and for the solid reasons given above, a pure large cap portfolio should just have index funds. And that’s why we have a Capitalmind Passive Index portfolio.

Investment concept: A regular investment every month is how we would imagine investing in such a portfolio. Premium subscribers: Ask on Slack in #bonds-and-funds if you have any queries!

If you’re not a premium subscriber, join, probably the best investment community in India.

As a Capitalmind Premium subscriber, get immediate access to:

- Model Portfolios: Three Equity and One Fixed Income

- Active Strategies: Chase (Our NIFTY + Futures long-short trend-following strategy) & other short-term actionable ideas

- Premium research: Priority access to our research

- Vibrant learning community on Capitalmind slack: Ask questions, share insights with a diverse community of newbie and veteran investors & traders