Under the right circumstances, groups are remarkably intelligent.

-James Surowiecki , Author of The Wisdom of Crowds

The Capitalmind Slack forum started back in 2015, primarily as a means for the CM team to communicate with subscribers about portfolio actions and short-term actionable ideas. Little did we know it would become the vibrant community it is today, with over 20 topic channels where over 1,400 subscribers exchange over 10,000 messages / day, on all things investing, trading, and quite a bit more (there is a #world-markets channel, and even a #geek-stuff channel). Newbie investors starting out, experienced traders and investors, industry veterans. And that diversity leads to incredibly rich discussions.

Read more about our amazing community here: A tucked-away treasure trove

We recently started a series called #StockOfTheWeek where we pick a company each week to discuss in detail, starting from the very basics and moving to the nuances.

This post offers a short summary of a #StockOfTheWeek discussion. The company – Bajaj Finance

Background

Bajaj Finance started as a captive financier for Bajaj Auto. In 2008, Bajaj Auto was demerged into 3 different companies:

- Bajaj Auto

- Bajaj Finserv &

- Bajaj Finance.

Slowly Bajaj Finance started to diversify its book from 2&3 wheeler financing into other areas like Construction financing, LAP, Developer financing etc. But things didn’t go as expected. After 2008 crisis, they took a big hit on their book.

The Mentor

Late Mr. Nanoo Pamnani (Ex-Citi bank India CEO & relative of Bajaj family) joined the board of Bajaj Finserv as Vice-chairman.

During the same time, Citi Bank India had decided to shut down its consumer lending business (Citi Financials) due to the bad loans of 2008.

This had created a void in the market. Mr. Pamnani, Mr. Sanjiv Bajaj & Mr. Rajiv Jain had seen an opportunity. First they cleaned up the legacy book. Took a hit & started focusing on consumer & retail lending like Personal loans, Consumer durable financing, Mortgage.

Since then they expanded into many areas of lending like SME, Commercial financing, Rural, Brokerage etc.

Consumer lending was further fueled by the introduction of Zero EMI. It was an instant hit as it’s a win-win for manufacturer, retailer & financier.

- Deepak explains how this works. Read this wonderful post here

In Numbers

They have 1.43L Cr AUM as of Q3FY21.

AUM Break up

- Consumer B2B: 18.7%

- Consumer B2C: 20.2%

- Rural: 9.1%

- SME Lending: 13%

- Commercial lending: 8.7%

- Mortgages: 32.3%

How things are looking Post Covid?

Pro-forma GNPA is at 2.86% & Net NPA at 1.22%.

Even after major write offs, they are well capitalised with CAR ratio 28.1% & Tier 1 capital of 24.7%. Thanks to 8,500 Cr QIP they did just before Covid.

All businesses are showing good traction except Auto finance. It is still at 62% of last year’s disbursements.

- Consumer (Urban): 86% of pre-covid volumes

- Consumption (Rural): 100%

- Credit card: 102%

- E-commerce: 107%

- Mortgages: 90%

- LAS: (-22%)

Cross sell stood at 64% of new loans compared with 68% last year same quarter. Cost of funds stood at 7.78% as of Q3FY21.

The company did a one time write off of 1970 Cr for Covid. Total provisions for Q3 stood at 1352 Cr. Total PCR stood at 58%.

Company is in the process of launching Bajaj Pay. Yet another UPI app. Will it succeed? Having said that, BFL holds 11% stake in Mobikwik platform.

Management Commentary

- AUM growth to resume back to pre-covid levels by Q4FY21.

- Cost of Funds will move further south to 7.5%

- Management expects the NPAs to return back Pre-Covid levels by H1FY22, except in Auto finance.

The paradox of high valuation

- Investors are reluctant of high valued companies. This can be true for any other sector but Financials.

- Finance companies need to raise continuous capital for growth. Gruh Finance & Sundaram were exceptions here.

- If they trade at a low valuations, they need to dilute more equity to raise the capital. But if they trade at a higher valuations, the equity dilution will be less for the same amount of capital to be raised.

The important question to ask

- Will market re-rate the stock again?

- How long before we see AUM growth back to 25+% levels?

- Will it chase growth at the cost of asset quality?

- The potential for Bajaj Pay if they can crack it.

Let’s open the floor for discussions.

A peek into the discussion

Financials

Reader PV on NIMs & sustaining profitability:

- How are they looking from profitability pov? NIM, PAT and PAT growth etc?

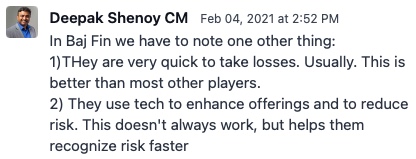

- CM view: NIMs will be sustainable at 9.5% to 10% because of lower cost of funds & change in liability franchise. ROA will be around 3.3%+ & ROE of 20% is sustainable. Management guided both AUM & PAT growth will be back to earlier (25-30%+) levels from next year. Historically they have beaten their guidance on AUM & Profitability.

Reader NS on Valuations:

- Bajaj finance is very strong franchise with great management, they have proved their prudent capital management / allocation approach specially during covid times the only real question is does the current valuation justify their ability to keep sustaining good quality growth. Have you done reverse DCF to reach at their current valuation? I mean what growth has market factored in current valuations.

- CM view: Actually DCF & Reverse DCF etc do not apply much in the case of Bajaj Finance (& many others like HDFC Bank). Mainly in current low interest rate regime. Key factor is the asset quality. We think as long as they maintain asset quality & prudent lending practices, growth will come back slowly.

Reader AK has a similar view:

- Answers for persistently high valuation can also sometimes be found in supremely favourable business characteristics: when companies enjoy a special position or privilege that allows them to make abnormal profits.

Profitability & future ahead

Reader M on Asset quality & peer comparison:

- What is the average cost of funds for Bajaj finance ? Was just thinking if npa numbers are masked by growth ? How is Bajaj finance compared to IDFC first as probably both are doing similar kind of loans but IDFC first has a banking platform?

- CM view: The average Cost of Funds is 7.78%. But incrementally they are borrowing at 7.5%. Since the growth is front loaded & risk is back ended in lending, there is always a risk of under reporting NPAs. But historically BF management is proactive in reporting the bad loans & providing or writing them off. We had seen the same during Demon, ILFS, Karvy fiasco & recently in Covid.

- Regarding IDFC First Bank, yes both are focusing on retail lending (along with many other players including Fin Techs). The issue with small ticket loans is that it all boils down to the underwriting. Rajiv Jain in one of his interview says, his profit is made on the last EMI. Also the tech enabled systems to assess the borrower credit worthiness, pre-approved loans, cross selling between 4.6 Cr customers & 1L touch points they have the scale. And from operations perspective, this scale helps them to bring down costs substantially. Opex to NII came down from 42% to 32.3% in just 2 years.

Reader AM on cost of funds & deposit rates:

- Their cost of funds could go down further, incoming deposit rates being offered by BF are close to 7% at max.

- CM view: Yes. Their Deposit book was zero around 7 years back. And now it contributes almost 24% which is commendable. But we think it will be in the range of 25-30% given their focus on maintaining diversity in the liability mix.

Bajaj Bank?

- CM view: Bajaj management is not so keen on Banking license because of:

- High regulatory compliance like CRR, SLR, Audits etc

- They have to dilute promoters share holding

- The advantage of low cost of funds is still there, but that will get compensated by the high upfront costs & Opex initially.

But, Reader H has a different opinion & a valid point:

- “The promoter is actually keen on getting the banking license (post some relaxation by RBI initial indication through a working paper currently). Sanjiv Bajaj has talked about it multiple times. Regulatory compliance does increase, but it gives a long runway to an NBFC which currently has ~1.5L Cr of assets with growth expectation of 25%+ in advances. Having stable liability side is most important for NBFC of such scale. Promoter shareholding dilution is a challenge but becoming a bank gives the promoter chance of stable wealth creation (Uday Kotak is a classic example). Also, with what has happened with IL&FS, Indiabulls housing and DHFL, RBI doesn’t want an NBFC to become as big and become a risk to the entire system; thus actually wants them to convert to a bank, and bring it under its purview. Few concerns on Bajaj Finance:

- The negative surprise came in Q1FY21 results when they talked about Flexi loan for the first time on their con-call; and the sheer quantum of the same. The book grew massively in Q1 and Q2 (Note: the management refrained from mentioning the quantum of outstanding Flexi-loan in Q3). The Flexi loan is an OD product offered by few banks also, but for Bajaj Finance the book currently stands at ~30-35% of the entire loan book. This is a very risky product since you only collect interest (no principal) for 1 or 2 years depending on your duration of loan.

- Mortgage (home loan + LAP) was the fastest-growing segment for them over the last 3-4 years. They have started hitting a roadblock on this specific product now (had large balance transfers in Q3FY21), since it has become difficult to compete with the likes of SBI, HDFC Ltd, LIC Housing, PSU Banks and now Kotak Bank; all of which have now become extremely aggressive in this segment.

- They are not big in e-Commerce in fact are losing market share to banks. Growth in eCommerce has been sharper specially during the covid period, and chances are if this sustains Bajaj Finance will have a tough time selling its EMI cards (primarily through offline outlets).

- Bajaj Finance is one of the most expensive stock among banks and NBFCs, and it was getting the premium for its growth and ability to maintain its asset quality; but this time when most banks have surprised positively on asset quality vs Q1 guidance; Bajaj Finance is actually on track to deliver the same outcome despite a sharp improvement in macro. Also, now it needs to find new product lines to have 25%+ growth in overall advances. This becomes a decent case for multiple de-rating going forward imo.”

House view on Bajaj Finance Management

- The strong part in their business model is adapting to digitalization of activities from product to consumer, specifically in retail lending. This gives a cutting edge on penetration & scalability, also giving rich consumer experience.

- What I really liked in bajaj finance is that they are constantly innovative in product offerings and the platform is really nice. If you think from a tech perspective, they are also trying to become a platform for other services and not limited to loans.

- Mgmt quality is excellent..i mean..Rajiv Jain..their IT teams etc.

- Have heard from banker friends that they are the best at cross selling, probably to do with the tech and analytics folks here talk about.

- BAF is becoming more of a fintech company and extremely agile in using technology to improve market share. They have survived the pandemic and in one of the interviews- promised it will be a different company at the end of the tunnel.

We’ve recently had #StockOfTheWeek discussions on IRCTC, Century Ply, Indus Towers, with many more to come.

Join the conversation. Get access to model portfolios, actionable strategies and of course, premium research. Actionable Insights. Better Investing.