Note: This is a post sponsored by DSP Blackrock Mutual Fund. Please do not treat this article as a recommendation; we aim to provide information and education about the concept of Stock Market Indexes and specifically, of an equal weighted one.

We speak of the Nifty and the Sensex and the Dow Jones Indexes, but what are they?

A stock market Index is a “barometer” of the market – a set of stocks that, when put together, give you a better understanding of how the market as a whole is moving. In other words, an Index is a way to get an insight on how the overall market is performing.

The New York Stock Exchange has the Dow Jones Index, which was created in 1896. The Bombay Stock Exchange is the oldest stock exchanges in Asia, but it was only in 1986 when we got a “Sensex”. Now we a bunch of them – with the Nifty 50 in India being the most popular.

So if you get a bunch of stocks in an index, do they all carry the same weight, or do you weigh them differently?

The Dow Jones Industrial Average was based on Price. This means that Boeing which trades at $240 has the highest weight in the Index while the smallest (in price terms) stock in the Dow – General Electric at $25 commands the lowest weight, at 1/10th the weight of Boeing.

But if one were to value the company based on its Market Capitalization, General Electric is actually 30% higher than Boeing! (GE has way more shares outstanding than Boeing)

To avoid this, most major Indices around the world use Market Capitalization to weight stocks, not Price.

Are Market Cap Indexes Okay?

Market Capitalization based indexing has issues. Some companies are fully owned by the public. In many others, Promoters hold the major part of the shareholding and won’t sell. A Wipro with 75% owned by promoters is not as easily tradeable as Infy where promoters own less than 20%.

So we go deeper. We can use Free Float Market Capitalization where stocks are weighted based on non-promoter holdings. This is how the Nifty 50, and the Sensex 30 are structured.

On the Nifty 50, the largest company by Market Capitalization is Reliance. But for weight in the index, HDFC Bank carries the largest weight. This is since Reliance Promoters hold 47% of its equity shares while HDFC Bank Promoters hold 26%. The “free float” of HDFC Bank is valued at higher than that of Reliance.

If you want the exact same return as an index, you simply buy stocks in the exact same weight. Over time, you “rebalance” to ensure that your portfolio has the same weights for each stock as the index itself. But buying 50 stocks and rebalancing is a major pain! How do you do it?

Enter the Index Fund

A mutual fund can do this for you. They take investors’ money, pool it together and buy stocks in proportion of the index.

The typical “Active” Mutual Fund has a dedicated Portfolio Manager with Analysts, who picks stocks. But Index funds are “passive”. They don’t do any research. They just track the index. No research means lower fees, and a fund manager has little real work to do.

In the developed world, active mutual funds were unable to deliver consistently better returns than a vanilla index fund. In those markets, it’s apparently difficult to beat the index primarily because fees eat up too much.

In 1976, John Bogle started the first Index Fund saying that rather than trying to beat the Index, this fund would mimic the Index and do so at a fraction of the fees that Mutual Funds charge. He started the fund management company popularly known as Vanguard. This is now one of the largest asset management companies in the world.

This is because Index funds have, in the developed west, outperformed most actively managed funds, largely due to a lower fee structure. And this has attracted money into index funds, as much as $90 billion a year.

India’s different. We’ll speak about that.

In India: Index Funds and Exchange Traded Funds

In India, you can buy index funds directly from a fund house. Or you can buy some on the exchange, which are called Exchange traded funds (ETFs).

Index Funds have a single price for the day (if you buy today morning, you’ll pay for the value of the fund at end-of-trading day today), But ETFs are available for purchase through the day. You’ll need a demat account to buy an ETF, though – and an index fund can be bought without one.

In India, Exchange traded Funds suffer from low liquidity, so you could end up paying a lot more than the value of the fund.

In the battle between ETFs and Index funds, it’s the index funds that offer a simpler way to buy and sell, and cost about as much or lower.

At last count, there are more than 28 Index funds. All combined, the Asset Under Management comes to barely 7200+ Crores, a miniscule number when looked at the context of total assets under management in Active funds (which have more than Rs. 500,000 cr. in Assets)

Why is so much money with active funds? The answer is simple: most active funds are able to beat the index! In the west, active funds struggle to beat broad indexes. India’s relatively inefficient markets and index structure means

However, if we look at the trend and comparison with foreign indexes, this could change. And it may be in your best interest to be ready for that change, if active managers being to underperform.

Smart Beta

Let’s say you want to beat the index. But you don’t want to spend time in actually researching stocks. Can you just invest in the same index stocks in a different way?

Smart Beta is just that. Rather than weighting the stocks based on Market Capitalization, Smart Beta is about weighing the stocks differently.

Some of the major ways Smart Beta weights stocks are :

- Dividend Yield

- Equal Weight

- Growth

- Beta

- Low Volatility

- Momentum

- Quality

- Small Size

- Value

Smart Beta is fairly new but has seen a growing trend over the last few years. In 2010, Motilal Oswal Mutual Fund launched MOSt Shares M50 – India’s 1st fundamentally weighted ETF based on Nifty. In 2014, after multiple years of underperformance of Market Capitalization based ETF’s, the fund shifted course and converted to being a normal ETF from a Smart Beta ETF.

The Equal Weighted Index

Of specific interest is the “Equal Weight” category.

You just weigh all the index elements equally. So if you’re buying an index of 10 stocks, you put 10% in each stock. That’s a simple way to look at it, but it does something quite interesting.

In regime changes, the lower market capitalization stocks grow bigger and replace the highest ones. An Eicher will replace a TVS Motors, and a Bajaj Finance will replace a Reliance Capital. Over time, the small companies become bigger. If you give a low weight to low market-capitalization stocks, you will obviously have lesser money invested in them compared to the higher market-cap stocks.

But what if you invest in them equally? The lower market-cap stock grows faster and the gains in it are much more than the flat or losing trade in the higher-market cap stock. This limits your losses and increases your gains.

An equal weighted index does just that – invests in all stocks equally. And then, market prices will change, so every few months, it will “rebalance” to get you to equal weighted again.

Tell Us More About Regime Change

In the current Nifty 50, HDFC Bank has a weight in Nifty 50 is 9.24%. This is so big that it’s as much as adding up the weights of 16 of the lowest weighted stocks!

In other words, a 1% move up in HDFC Bank can compensate for a 1% move in every one of the 16 low weight stocks. That’s because of HDFC Bank’s huge free float market capitalization.

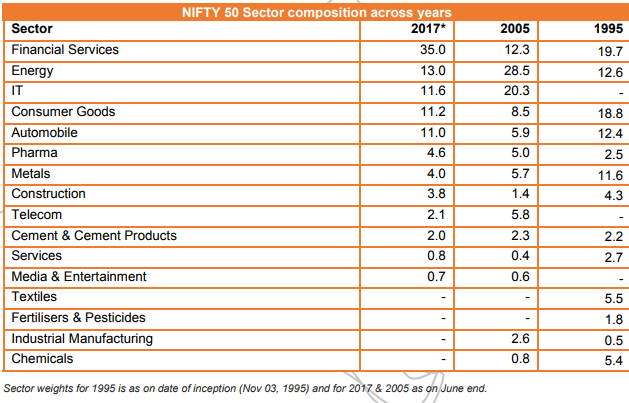

Currently Banking Sector constitutes the highest weight at 27% with the next largest sector in Index being Software at 11.42%. But this is not static. Here is a table of sector weights at different times.

What the above table showcases is Regime Change. What is currently the best may not remain the best. The Metal sector had a weight of 11.6% in 1995. Two decades later, the weight is down to 4%. Textiles which used to command a weight of 5.5% in 1995 isn’t even represented in the Index now.

St1ocks and Sectors are prone to mean reversion over longer periods of time. At such times, a Market Cap Weighted Index may not be the best way for exposure to stocks in a specific Index.

An equal weighted index performs well in such times of a regime change. And India seems to be there now. From the heavily weighted banks and metal/oil companies, India’s story is changing; the leaders of the next 10 years are likely to come from different sectors. Exposure to stocks in an “equal weighted” fashion could do much better than the Nifty itself.

How do you invest in an equal weighted Index?

It’s not like investing in them is easy. Buying 50 stocks equally is fine – put 2% in each stock. But a stock like Bosch in the Nifty requires Rs. 20,000+ of investment, so your investment needs to be at least Rs. 10 lakh. That’s too much for most people.

Enter the Equal Weighted Index Mutual Fund. They take money from a lot of investors and buy the equal weighted index in a pooled fashion. A new addition to this will be the forthcoming DSP BlackRock Equal NIFTY 50 Fund. This tracks the Nifty in an Equal Weighted Fashion.

The Fund will have two options – Regular (where the fund pays commissions) and Direct (where it does not). The idea is to track the Nifty 50 Equal Weighted Index more closely, and they intend to charge 0.4% management fees (Direct) and 0.9% fees (Regular).

Being different doesn’t mean this fund will out-perform and as we shall see in the next post, there are large periods of time where this index has under-performed a market capitalized fund due to the way the portfolio is structured. But if the statistics in the west hold true, equal weighted index funds are likely to create outperformance, especially in India where regime changes are common and likely.

Performance: A Quick Note

We’ll have more on performance, but the Nifty 50 equal weighted index should be looked at with these eyes:

- Rolling returns of five years, to avoid starting point bias. We use this to avoid, say, five year return comparisons, because a different starting point can dramatically change the conclusion.

- Use only “Total” returns, where the analysis includes reinvestment of dividends. This is the best way to compare returns.

The Nifty 50 Equal Weight Index has a 95% correlation with Nifty 50. This means that returns will be similar in nature. The chart below plots the 5 year rolling return comparison:

As you can see, we’ve had large periods of outperformance in the 2000s, and where markets were between 2009 and 2013. However, for the four year period after that, we saw a lower performance by the equal weighted index; this is mostly because the stronger stocks in the index (ITC, HDFC Bank etc.) rose more, and the smaller stocks fell.

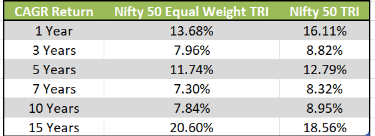

They also differ in draw-downs with Nifty 50 Equal Weight having seen a Worst case drawdown of 57.50% versus the Market Cap Weighted version having a drawdown of 58.50%. Current 5 year returns are around 11.7% for the Equal weighted fund, versus 12.79% for the regular Nifty.

In the last five years there wasn’t that much of a regime change – it was the heavyweights that got heavier.

Our View: It’s Good To Have Exposure.

Note: This part is purely Capitalmind’s view. There is no sponsor input here.

At best, this kind of an index investment should be less than 10% of a portfolio, because active funds still outperform the index. When that changes, it will be time to increase the allocation to such indexes.

More posts coming up. There is a new fund offer for the DSP Black Rock Equal Nifty 50 Fund in progress. Capitalmind is being compensated for writing this post, so please assume our bias. We will have more details on such index performance in subsequent posts, but please do note that past performance may not be repeated. Please note: The views & opinions expressed in the article are that of the author and not of the sponsor.

Disclosure: Capitalmind is now a SEBI Registered Portfolio Manager.