Here is another interesting stock from our proprietary SNAP Outliers – our discovery tool for stocks with momentum. Catch them all here.

![]()

Today we look at EID Parry [check out the action on snap here]

![]()

One of the earliest in the Industry, EID Parry – part of the Murugappa Group of Companies – is a leading manufacturer of low cost sugar. EID Parry also made its mark in the areas of Bio Pesticides and Nutraceuticals.

With over 40% of the sugar sales (volumes) coming in from Institutional segment, EID is a major supplier of raw material to the Pharma Industry. Manufacturers of soft drinks, beverage, food, confectionery, dairy, biscuit, and ice cream also form part of the company’s customers.

EID has 9 sugar mills spread across Tamil Nadu, Puducherry, Andhra Pradesh and Karnataka. The company also has a standalone distillery in Sivaganga.

EID has the capacity to crush stands at 43,700 Tonnes of cane per day, generate 160 MW of power and distilleries with a capacity of 234 KLPD.

1Q results

- Sugar operations reported an operating loss of Rs. 22 crore against a profit of Rs. 57 crore.

- Farm inputs reported an operating profit of Rs. 183 crore against Rs. 92 crore.

- Bio-products division reported an operating loss of Rs. 1 crore against a profit of Rs. 8 crore.

Takeaways from 1Q results

[includes the numbers from the merged Parry’s Sugar Industries]

- Performance impacted by the drop-in cane availability [fall of 89%] for Tamil Nadu [a higher impact since this is where the company’s operations are setup – Tamil Nadu has the advantage of good soil conditions and abundant water with sugarcane yield being highest across India].

- Sugar realization prices jumped 17% YoY. Bio Pesticides witnessed an impact due to a significant increase in neem seeds price

- Higher cost of seed material left an impact on the profitability of the bio business.

- Rs. 12 crore set aside to de-bottleneck 4-5 sugar plants. 3Q is when the 3 units in Karnataka and a single one in Andhra Pradesh come to life. De-bottlenecking will cost Rs. 4-5 crore which will increase the capacity from the current 6 lakh tons to 7 lakh tons.

- Short term Debt stands at Rs. 100 crore while Long Term stands at Rs. 720 crore. Average service cost is close to 7%.

- FY18 expectation of crushed cane would witness a 12% to 14% drop in terms of availability. FY17 numbers stood at 44.5 lakhs tons.

- Demonetization has impacted realizations of property prices and hence the company is slow in monetizing some of the properties.

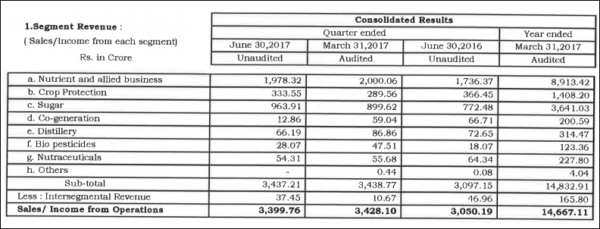

- Consolidated Revenue stood at Rs. 3,430.25 crore against Rs. 3,075.53 crore while Profit after Tax measured at 20.33 crore against Rs. 18.90 crore.

Here is what the Managing Director – S Suresh had to say:

The performance of the company in Q1 has been largely impacted by 89% drop in cane availability in Tamilnadu due to the prevailing drought conditions. This has had a cascading effect on the production and sale of sugar, power and alochol. The above impact has been mitigated to some extent by better realization of sugar price by 17% compared to the corresponding quarter of previous year. In addition, the company has imported raw sugar, allotted by the Government under the TRQ (Tariff Rate Quota) which will help in sugar availability for sales. We expect the sugar prices to remain firm for the year 2017-18.

Big Whales

With promoter holding at 44.99%, Big Whale investors Hitesh Satishchandra Doshi and Nemish Shah each hold 1.29% and 1.18% respectively.

Holdings of Foreign Portfolio Investors stands at close to 9.6% with General Insurance companies holding another 5.5%.

Price Action

Being a cyclic industry, EID Parry has a strong correlation to the underlying commodity – in this case Sugar. Sugar hit a all time high in 2011 and was in a strong corrective mode till mid 2015. While the rally of 2015 has cooled off, strong prices along with a lower yield in India meant better prices for Sugar.

Thanks to its other diversification, performance of EID Parry has been better compared to pure Sugar Mills. The stock broke above its high of 2010 in May of this year and after a period of consolidation seems ready for the next phase.

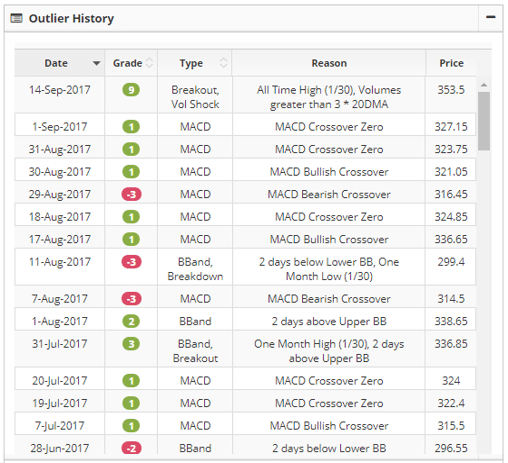

Outlier History:

Outlook

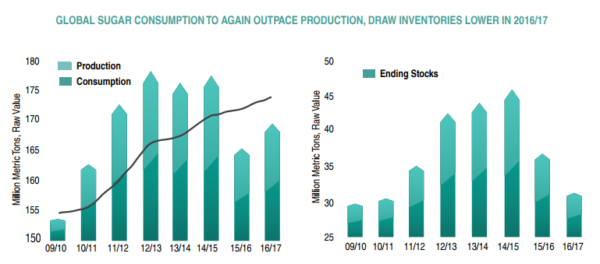

- An estimated increase of 70% in sugar output in Maharashtra in 2017-18 is expected to balance the country’s overall sugar production to near consumption levels.

- Lower realizations expected up to the end of 2Q with the stock holding limit for trade on sugar.

- ICRA report confirms the fact that the western and southern mills would continue to be impacted by low cane crushing volumes while good sugar prices are likely to support the profitability of the UP-based sugar mills.

NOTE: Please do not consider this article as a recommendation, It is purely for informative purpose only. Authors may have positions in the stocks mentioned, so consider our analysis biased. There is no commercial relationship between Capitalmind and the companies mentioned in this analysis.