The current genre of stock investors may not even have seen a share certificate let alone traded during the 90s or earlier. For the longest period of time, a physical share certificate was proof of ownership of a stock. Of course, while on paper this is good, it created huge problems for both investors and stock brokers, not to speak about loopholes that were maximized by certain fraudsters’ intent on duping the public.

A physical share certificate suffered from several faults: the main thing was the time it took to transfer stock from one person to another. Depending on the company, this could range anywhere from a month to forever. And then, you might get forged certificates. Or you may want to sell 50 shares, but have a certificate for 100 – so you first contact the company to split the certificate into two certificates of 50 each, which could take a month or more, and then sell to transfer, which is another month. These were interesting times indeed.

With growing volume of transactions on the exchanges, SEBI felt the need to move towards converting the physical to digital. Meaning: Use a source of truth: the “depository” where all shares would be stored digitally, with ownership information. Moving owners was just about changing a few bits and bytes.

The History

India wasn’t the first country to face such issues. The earliest Depository execution was in Germany during the late 18th Century. The real movement though started in the 1960’s when United States moved towards eliminating physical share certificate and replace the same with accounting entries (like a passbook).

In 1995, SEBI created the ”The Depositories Act, 1996”. Post the Act, National Stock Exchange of India set up with a host of other entities including “National Securities Depository Limited (NSDL)”.

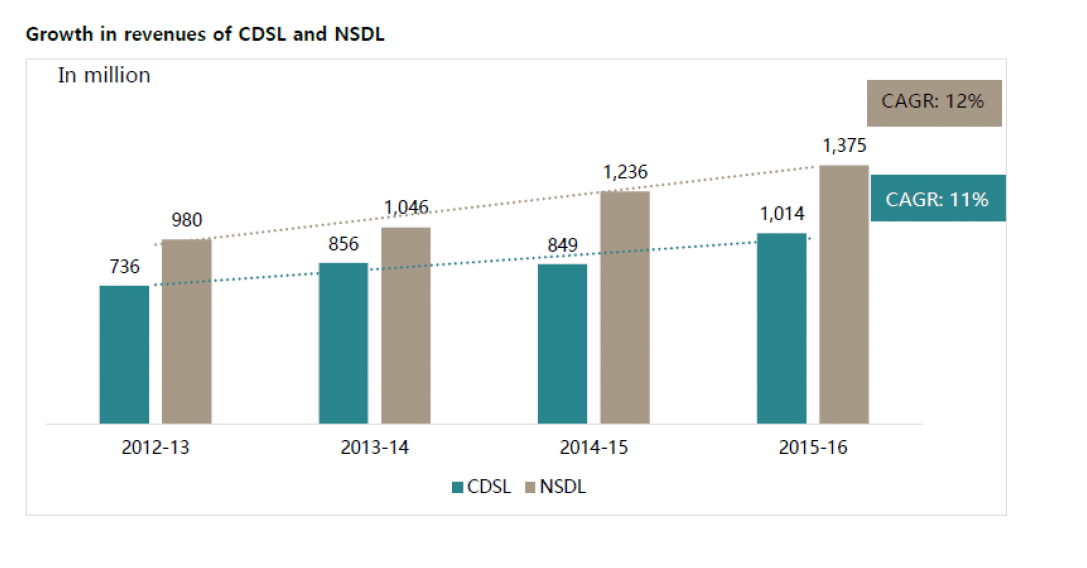

For the first three years, NDSL had its run of the house and took full advantage of the “first mover advantage” Later came CDSL, promoted by BSE in 1999. NSDL has been able to hold on to 58% of the share of revenues even now, which means the market’s more or less even.

Value of securities held in NSDL system as on January 19, 2017 was ₹134 lakh crore (US$ 1.96 trillion) which represents 90% market share in custody value, 97% in debt securities and over 99% in terms of Foreign Portfolio Investment in India. CDSL is smaller at about Rs. 18 lakh crore worth of securities.

The Offer

Bombay Stock Exchange along with State Bank of India, Bank of Baroda and Calcutta Stock Exchange is now offering for sale 35,167,208 equity shares of CDSL at a price band of 145 – 149 per share.

Of this 27 million shares will be sold by BSE. This is purely an offer for sale, so no money goes to the company, only to selling shareholders. The company has 104 million shares, so around 35% is being offered to the public, for around Rs. 520 cr.

Valuation

CDSL mainly earns fees out of charges for annual maintenance and a fee for every transaction out of the depository.

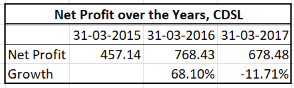

For the year ended 31st March 2017, the company earned Rs.8.21 per share (Earnings per Share). Earnings have fallen a bit, from Rs. 8.71 for FY 2016. At the upper band of 149, this would translate to a Price Earnings Ratio of 18 times its earnings. Profits for the year saw a decline of 4% compared to the Profit after Tax for the year ended 31st March 2016.

CDSL’s market cap at a price of Rs. 149 per share will be Rs. 1550 cr. which means it’s a P/E of about 18. A 25 P/E is high for a company that’s not growing, but it’s a company in an area where there is only one major competitor, and no one else in the fray.

CDSL has about a 44% market share in terms of number of demat accounts but has only a fraction of the value of shares of NSDL. However, most fees are fixed rather than a percentage of value, so the number of accounts matter more than the value inside them.

Bombay Stock Exchange has been reducing its stake either by sale of its holding or dilution by further issue of shares and post issue it stake will slip to 24%. A market cap of Rs. 1550 cr. means the BSE will hold around Rs. 370 cr. worth of CDSL, but at the same time, it will cash out Rs. 400 cr. by selling CDSL Shares in the IPO.

They key driver for growth of both NSDL and CDSL has been due to the backing it has received from the stock exchange and the broker community associated with it. Even after the Offer for Sale, it will remain as the key driver with management control.

The biggest advantage for both NDSL and CDSL is the fact that its very much unlikely to see a competitor and in a duopoly that would ensure that there is no cut throat competition that could lead to losses.

On the other hand, markets have matured which means that growth will be more flattish in nature and in line with Inflation+ .

The big question, Is it worth subscribing to the Issue?

Since NSDL, the only other depository isn’t listed, we don’t have much of comparison on what the market values companies like these at.

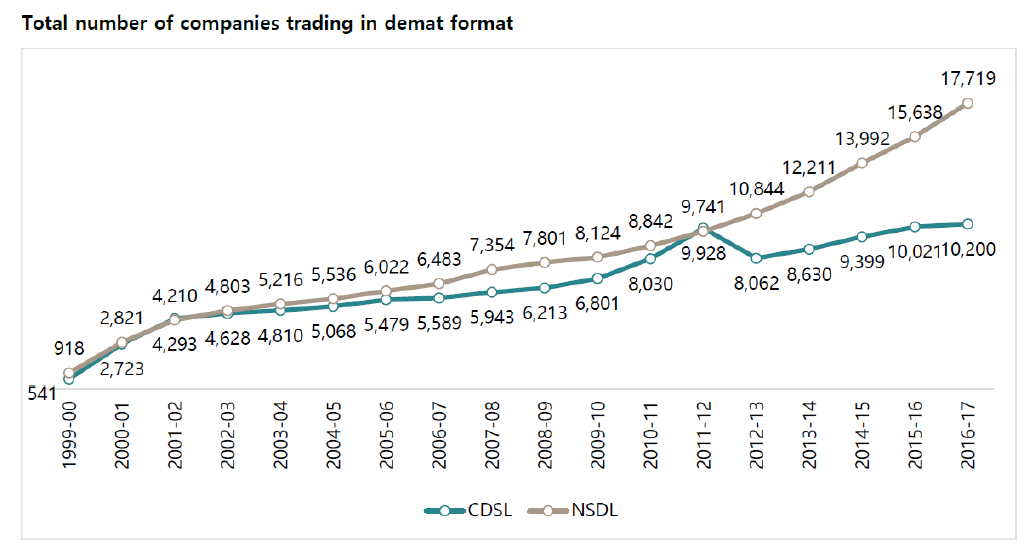

Over the last 15 years, CDSL has seen an increase in depositories at 10% (CAGR) verus NDSL’s 1%. On the other hand, starting from 2011-12 when both CDSL and NSDL had more or less the same number of companies listed with them, NSDL now controls 63% while CDSL remains a laggard.

Much of the applications these days for Initial Public Offers target the opening pop. The same could be true for CDSL too. Post the listing; the stock could be looked at more as an Annuity product that pays out a regular dividend than a stock that offers superior growth. In other words, this issue is one of a boring business but one that is priced moderated aggressively.

There are some positive triggers on the stock. For one, that the RBI will allow faster movement of government bonds into demat accounts – this will increase the size of the demat universe. Second, that there are new types of securities coming – from REITs to InvITs to bonds – which will increase the need for demat accounts.

However the growth is likely to be in the single digit percentages, which means paying a big P/E (18) for low growth. In a lot of ways, the duopoly of CDSL/NSDL plays in its favour and offsets the need to grow really big.

But there is a lot of demand. We will not recommend the stock – recommendations are useless, because either you get allocation because no one wants it (bad) or you get no allocation (bad). Current IPOs want to allocate to the maximum number of investors. So if you want to apply, just apply for one lot – a big oversubscription means that’s the max you’ll get.

Note: There is an impact on the BSE IPO too, which has a market cap of Rs. 5,800 cr. currently. They’ll see income of Rs. 400 cr. from the IPO, which should mean a decent dividend. They’ll also continue to hold 24%. However, BSE has very little else right now, and volumes are still thin, so the CDSL holding may just be its redeeming virtue. We expect that stock to move up if the listing of CDSL is much higher than the IPO Price.