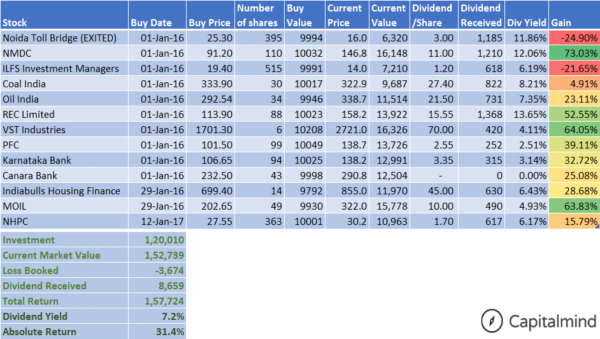

The Dividend Yield Portfolio has been doing well with a 31% return since Jan 2016 (when we started it). And we had a 25% loss in one stock (Noida Toll Bridge) after the High Court yanked off the carpet from below it, by banning tolls on the only bridge it runs.

And what we replaced it with – NHPC in Jan 2017 – saw a return of nearly 16% in two months, thanks to a nice 6% dividend yield we anticipated that day.

The rest of the portfolio has done brilliantly. An equal weighted purchase at the beginning would have resulted in a return of about 31%!

Just the dividend on the portfolio gave a 7.2% return, and the capital gains gave the rest.

The best performer was NMDC, closely followed by VST Industries and MOIL. We even saw a boring REC return 53%, including a dividend yield of 13.65%!

This has been an extraordinary performance for a portfolio that was expected to be boring and staid. Most players are owned by the government. Many others have chosen the buyback route instead of dividends (we didn’t account for any, though in two occasions it didn’t make sense at all since the market price was higher on the day of the buyback).

Karnataka bank has been adjusted for the rights issue.

What would we change?

The one stock we don’t like is Canara Bank, which has paid no dividends. Yes, a 25% return is good, but we need the stock to pay, otherwise it doesn’t belong here. It might need to be reconsidered.

IL&FS Investment Managers might need a rethink too. Although it will benefit from InvIT regulations, nothing’s really worked out too much for them. Profits are down substantially and they may not have enough in there to pay big dividends.

Plus, we have some hefty dividends from the oil marketing companies. HPCL already paid out Rs. 22.5 on a stock price of around Rs. 530 and they are likely to make over Rs. 60 per share this year in net profits. These might still look interesting to add.

New dividends may come from buyback opportunities, so we expect subdued performance from non-PSU stocks until this loophole is blocked in some way.

We will make changes in the dividend portfolio soon, and since it’s been a year from the start, there will be no capital gains on the profits. Watch #actionable on Slack.

The Point of a Dividend Portfolio

We don’t often mention this portfolio. It’s more about a long-term steady income performer, but this year was special. It’s a useful thing to own, just to make good dividends. Remember this – even if you consider zero portfolio gains, the investment has returned a 7.2% post-tax yield (dividends are tax free). That’s much better than what tax-free bonds provide, and hopefully over the long term, the stocks will retain enough juice to not lose capital.

Such a portfolio should be bought early (or regularly) and only reconsidered if there is a major event, or once a year or so.

While the stocks we have mentioned have run up considerably, most stocks remain a buy if you were to begin with this portfolio, except:

• Canara Bank, where we think we might replace it

• IL&FS Investment managers where the profits aren’t enough to pay big dividends now.

We’ll keep a track of changes in the next few months, and hopefully if there is a correction there will be a chance to add more of these stocks.

At Capitalmind we want to demonstrate how, in the longer term, a dividend yield portfolio could be built so that you can get better-than-fixed income returns from your stocks themselves. If a stock pays Rs. 10 today and you buy it at Rs. 200, you get 5%. But if it increases in value to Rs. 500 in five years, and the dividend paid out is Rs. 25 (because profits grew too) you will find that for your Rs. 200, you’re now getting 12.5% returns.

Stocks can actually give you higher yields because of this phenomenon – in other fixed income products, an interest rate is known and fixed for the duration of the investment. It’s useful to have a portion of your portfolio parked in such high-dividend stocks.

Our Premium Long Term Portfolio is at https://premium.capitalmind.in/capital-mind-long-term-portfolio/

Our Premium Momentum Portfolio 2.0 is https://premium.capitalmind.in/momentum-portfolio/

Note: This is not portfolio advice. Consider this a very risky portfolio and proceed at your own risk. At Capitalmind Premium the reason we have a portfolio is to demonstrate our commitment to our analysis, and we track it closely. It is not meant to be a recommendation for anyone in particular, primarily because we don’t know your risk profile.

Holdings: Analyst and family do own some of the positions listed above. Please assume we are biased.