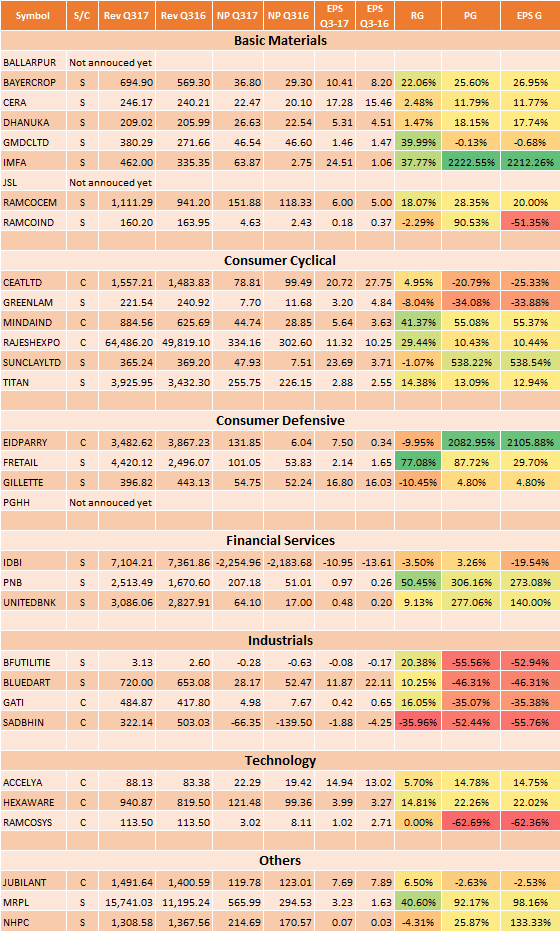

Here is a quick summary of the 3QFY17 financial results for all the companies announced till date. For some companies, management comments have been reported here. Additionally, please refer notes at the bottom.

You can catch the first part of the detailed results piece containing management comments for 18 different companies. In today’s results piece we have captured the management comments for the following 12 new companies i.e. Apollo Tyres, Asian Paints, Dabur India, Equitas Holdings, Finolex Industries, Godrej Consumer Products, Havells India, INOX Leisure, Jubilant Life Sciences, L&T Finance Holdings, Lupin and Teamlease Services.

Note from the Author

Last week, our publication titled “Earnings Report: 3QFY17 : 495 Companies Till Now With Management Comments” misrepresented a few numbers. We sincerely regret the error and have the rectified the values here.

Nifty

Upcoming Results

Sectoral Performance

Basic Materials

Asian Paints

- The decorative business registered low single digit volume growth in Q3. Demand was impacted on the back of demonetization, particularly in North and Central India. Sales in South India especially Tamil Nadu where affected due to the cyclone Vardah in the month of December.

- The Industrial business registered decent growth in the quarter due to a good pickup in the auto OEM segment. Industrial segment servicing mainly the 2-wheeler OEMs was affected due to the fallout of demonetization.

- The Home Improvement business growth was much slower than the earlier part of the year due to the effect of delayed sales.

- The International business reported good numbers specifically aided by contributions from Nepal, Fiji and certain units in the Middle East.

- We are in a more of a VUCA (volatility, uncertainty, complexity and ambiguity) world and we have to learn to live with these fluctuations in demand and the environment.

- Finished goods inventory that is kept in our retail channel partners – the average is somewhere between 15 to 30 days. 70% odd of the sales is done on cash payment. December sales were better than what we had in November.

- New capacities being set up other than in Ankleshwar will be only emulsion capacities. No facilities which are enjoying tax benefits.

- Disruptions that would follow post the implementation of GST – short-term disruptions because how stock in trade in the channels would get the credit for the various taxes, taxes already imposed. Second the GST rate that comes into implementation whether it significantly increases the prices or decreases the prices of paint, can affect demand of the organized sector versus the unorganized sector.

Communication Services

Consumer Cyclical

Apollo Tyres

- A margin drop on a year-on-year basis was due to the cascading effect of the price cuts undertaken.

- Raw material prices on a sequential basis was marginally up by 1%. Price hike taken in January was 1% to 1.5% in farm category. The company is considering to increase prices going forward in the light of rising raw material prices.

- 3/4th of the revenues come from the replacement market and one-fourth from the OE. Truck tyres category contribute 43% to revenues, passenger car tyres 40%, and the balance being made up of light truck, farm and other categories. There was significant increase in new vehicle registration.

- Going forward, one of the challenges remain rising raw material prices that is expected to increase by nearly 10% in coming quarters.

- Though the impact of demonetisation was felt in December, overall the quarter was managed quite well. One good point for the company was that the demonetisation also impacted the Chinese imports. The imports might have dropped from about 150,000 per month pre-demonetisation to about 100,000 per month currently.

- The Hungary plant continues to progress on track and would be starting production in the current quarter. The total capacity at the end of phase 1 would be 16,000 passenger car tyres a day and about 2,000 truck tyres a day, which would be reached by end 2019. The production would begin towards end of this quarter and the ramp up would happen over the next two to two-and-a-half years. Capex is €300 million. The agreement with the EU authorities has resulted in total cash subsidy of about €52 million on an investment of €475 million and we have already received about €15 million.

- Two-wheeler tyre business ramping up – did not see the expected ramp up with some of the impact of demonetisation. 90% of our revenue is domestic and about 10% exports.

Finolex Industries

- Volume of pipes and fittings was low by 3.5% due to the effect of demonetization.

- The budget for the year 2017-2018 has made allocations to agriculture, housing and infrastructure sectors, which will benefit the pipes and fitting industry. On 9th November we already started making plans for expansion since now is the best time to grow.

- January has been much better than December. We are still not back to what we would have done because this year the monsoon was very good. We were not able to pass on the full price of raw material hike to consumers.

- Volume sales for PVC fittings is 3,300 MT or Rs. 59 crore, PVC pipe is 37,600 MT and PVC resin external is 25,000 MT, CPVC pipes is 729 tonnes (Rs. 13.8 crore) and CPVC fittings is 148 tonnes (Rs. 9.7 crore) .

- Supply of PVC for this quarter is going to be tight in the market that is because of various reasons like shutdowns and things like that, imports not having coming in because of demon, so that is why I think first quarter this year, I mean last quarter of this year, prices have started firming up and will keep on firming up.

- Most of our inventory about Rs.150 Crores has gone up because of resin as we pulled back on the production of pipes, so we had a build-up of inventory in PVC and the reason we do not push it off so much because we were anticipating as it seems to be right that the price will start moving up and now the prices have started going up in January.

- Capex plan for FY17 and FY18 would be Rs. 50 crore roughly. Company has 1500 SKU’s of which 100 were added this year.

- We are evaluating whether to setup a new plant or a new warehouse, because in a new warehouse the advantages it is only variable cost, in a new plant it is huge fixed cost.

INOX Leisure

- Reason for shrink in EBITDA margins due to 2 reasons – one obviously the demonetization which led to some curtailment in both consumers as well as advertisement spending as well as indifferent content continuing in this quarter as well.

- Overall advertising minutes have gone down, no doubt, by roughly about 15%, but they still continue to remain fairly strong in relation to what we would have otherwise expected.

Four key segments

- Net box office revenue fell by about 3% in this quarter from Rs 181.6 Crores to Rs 176.4 Crores.

- F&B revenues increased by 3% from Rs 65.5 Crores to Rs 67.6 Crores.

- Advertising income increased by 2% from Rs 29.5 Crores to Rs 30.2 Crores, and

- Other operating income increased by 11% from Rs 21.3 Crores to Rs 23.7 Crores.

Some of the movies did well in this quarter. The top five grossers contributed 53% of the gross box office revenues:

- Dangal which had footfalls of 21.72 lakhs and a gross box office collection of Rs 47.45 Crores,

- Ae Dil Hai Mushkil footfalls of 10.76 lakhs and GBOC of Rs 22.66 Crores,

- MS Dhoni – The Untold Story footfalls of 11.97 lakhs and GBOC of Rs 20.76 Crores,

- Dear Zindagi footfalls of 9.19 lakhs and GBOC of Rs 16.92 Crores and

- Shivaay footfalls of 6.99 lakhs and GBOC of Rs 13.36 Crores.

Seven movies that were expected to do well did not perform that well at the box office

- Footfalls fell by about 3% from 129 lakhs in Q3 FY16 to 125 lakhs in Q3 FY17, Occupancies fell from 28% to 26%, and Average ticket price went up by 1% from Rs.179 in Q3 FY16 to Rs.182 in Q3 FY17. A lot of movies that were expected to do quite well did not perform that well and hence we could not have increased ticket prices.

- Distributor share on NBOC stood at 45.7% due to indifferent content, shorter duration of films, and distributor share for the first week is higher.

- Content pipeline going forward looks extremely encouraging. 2 expected block blusters being released – Raees, a Shahrukh Khan movie and Kaabil, a Hrithik Roshan movie. In February, we have Kung Fu Yoga, a Jackie Chan movie and Jolly LLB 2. These are followed by Rangoon, Commando 2, Badrinath Ki Dulhania, and Sarkar 3. In April its Jagga Jasoos, Fast & Furious 8 and Baahubali the Conclusion.

- Footfalls are down 10%, but occupancy is only down from just about 28% to 27% – that is just because the length of the movies was longer and hence we had fewer shows per day.

- Non-cash payments or digital payments – Q1 was roughly about 43%, Q2 was about 44% and Q3 was 61%.

Consumer Defensive

Dabur

- Sales in December did pick up but not fully as trade and wholesale channels continued to remain stressed and replenishment of cash was slow. Volume decline of 5% for the Domestic FMCG business.

- Massive down-stocking both at the distributor and trade levels, particularly in rural and northern and central India as these regions were more dependent upon cash. Volume de-growth is almost entirely a consequence of destocking.

- Multiple headwinds in international business with currencies devaluation in Egypt and Turkey accompanied by geopolitical and macroeconomic challenges in the MENA region.

- Destocking of the channels by around Rs.100 crores during the quarter, reflecting around 10 to 12 days of inventory reduction in trade pipelines. Distributor is sitting on 22 to 25 days inventories.

- Red paste and the Meswak brand both continue to grow quite well despite issues of demonetization. Red franchise is substantially urban, Meswak is almost entirely urban.

- Honey availability is plentiful, there is no economic case to increase the price.

- We are not going to see strong growths emerging in next few months. It will take longer for the trade to rebalance.

There is a little bit of overhang of GST because it is going to get very messy after that in terms of input credits and others.

Godrej Consumer Products

- The shortage of currency, particularly in the first few weeks of the announcement of demonetisation, had an adverse impact on demand. Staples and essentials were relatively less impacted and the impact was felt much more in the East and the North. Post demonetisation, we see an opportunity to gain market share from unorganised players and further strengthen our distribution for Expert Crème. More discretionary categories like air fresheners, toiletries saw bigger impacts.

- Indonesia’s performance was relatively soft due to the performance of our household insecticides business. Africa business continues to consistently deliver double-digit constant currency growth.

- GST implementation will lead to a significant boost to GDP growth and improved consumer demand.

- Postponed some advertising for about three weeks from the last week of November to mid-December.

- Expect soaps volume performance to be better in Q4 FY17 as compared to Q3 FY17.

- Stock levels are at historic low at least over last three years.

Energy

Financial Services

Equitas Holdings

- Operating environment was a bit challenging during the latter part on the quarter hence this has affected the disbursements and collections especially in the Micro Finance operations of the bank.

- Enhanced provision cover for the NPA during the quarter had led to lower PAT growth.

- On course to complete the roll out of 412 new liability branches.

- Our deposits as of December 2016 stood at Rs.760 crore, out of which about just under Rs.20 crore was CASA deposits.

- In Q3, there was an impact in a few States where we operate, where the Micro Finance industry went through certain levels of stress.

- Our Micro Finance collection efficiency for the quarter was 98.4% which is of course lower than 99.5%, till September. December it is 96.31%.

- In States of Karnataka and Madhya Pradesh, the rate at which the defaults were there has now kind of stopped, and almost come to a normal situation where further defaults are not taking place.

- Vehicle portfolio – some issue on the movement of goods due to demonetisation. Two-wheeler is not something where we are pursuing as target, it is just an offering which is there available only for the Micro Finance clients who wish to avail a two-wheeler, as we know these clients for almost two to four years. The ticket size is not more than Rs. 50,000 to Rs. 60,000.

- Loan against the gold – there is a substantial opportunity especially the agri-gold loan.

- Our intent is that over the next 3 years by maybe 2019, Micro Finance should be about a third of the overall book and the remaining being other products.

- Post conversion to a bank we were not in a position to do securitisation.

L&T Finance Holdings

- Q3, was a very strange quarter. First 38 days of the quarter were the best we have seen in the last three years, in terms of business, in terms of collection efficiency, everything. And the remaining 52 days were difficult, to say the least. In various businesses farm, housing, microfinance, we faced significant difficulties.

- Difficulties are not over – there are some of the difficulties of demonetization along with other difficulties will continue in Q4.

- Small impact overall in collection efficiencies – for December it stood at 98.11%. Today it is again close to 99%, which actually shows that the large part of the problem is actually not due to demonetization. We had actually said that the demonetization problem, we do not see as a big problem but is just Rs. 1,300 per instalment and we do not see a big issue.

- Two-wheeler business – collection efficiency not affected. Market share doubled from 4% odd to 8% odd. We have achieved all time high disbursements of Rs. 550 Crore.

- Farm disbursements – market share which had reached its lowest in Q2 has now gone up to more than 8%. Overall rural NPAs were 8.36% in Q2.

- NPA number on rural was 8.36% in September. We have reported a 7.96% after taking into account the impact of demonetization and this is close to about 170 crore.

- Home loans – retail home loans the pickup has come down. We disbursed close to Rs. 700 crore vis-à-vis the expected run rate of around Rs. 900 crore to Rs. 950 crore.

- Developer loans medium ticket size stood at Rs. 150 crore to Rs. 200 crore.

Healthcare

Jubilant Life Sciences

- Strong performance in our Specialty Pharmaceuticals business where revenues grew 26% YoY and which now contributes 56% of our Pharma segment revenues.

- Turnaround in performance has been on account of strengthening operations in our core business

- Orphan Drug – I-131 MIBG has been already given orphan drug status by USFDA and the product has already been supplied under USFDA program to hospitals for Neuroblastoma which is a cancer. So we are going to start the clinical trial sometime and the trial would take some time and I think by the time we get product approval it will take at least two years. If the patient results are good, then USFDA has agreed for expedited approval on this product.

- US market at the moment, there is overall consolidation of customer base in generics business.

Pharmaceuticals Segment

- Revenues from North America at Rs. 529 Crore, up 9% YoY and contributing 67% to revenues

- Revenues from Europe and Japan were at Rs. 138 Crore, up 47% YoY and contributing 18% to revenues

- Revenues from Rest of the World stood at Rs. 79 crore, up 17% YoY and contributing 10% to revenues

- India Revenues at Rs. 39 Crore, contributing 5% to the revenues

- Completed USFDA inspection at CMO Montreal and Radiopharmaceuticals facilities during the quarter

- Signed long-term contracts in Radiopharmaceuticals business with distribution networks in the US to supply products over a period of 39 months effective from January 2017.

- Rubyfill remains on track for US launch in Q4 FY17. Rubyfill in 4-5-years’ time the market size can be as high as $250 million.

- Received six ANDA approvals till Q3FY17 and plan to file about eight ANDAs during FY17

Lupin

- Growth is reflected across all our geographies – US with 58%, Japan was 19%, LATAM at 33%, India despite the demonetization is growing by 12% and EMEA by 17%.

- Some beneficial impact coming in from forex of Rs. 27 crores and of course R&D down by about 0.7%.

- US growth driven by growth in products like Glumetza. Fortamet obviously had additional competition of Mylan through the quarter. Somerset front growth was led by Methergine where the brand business has gone up 25% or so. Fortamet – expect that Mylan would litigate on the Para IV and we would expect a potential Aurobindo launch in 30 months or thereafter.

- Glumetza has 75% of the market and 25% remained with the brand. Expect Sun and Teva to launch at some point over the next 12 months

- April onwards we will be back on 15% plus growth in India.

- 25+ products that we have the potential of launching in the next 12 months – Minastrin, Epzicom, Bupropion XL including ramping up Methergine. For Renvela and Welchol – had queries back from the FDA and we’re trying to address all of them comprehensively.

- US business pricing due to McKesson Walmart negotiations – price erosion at the high single-digit. Japan business pushback was on the reform that the government got on generic substitutions, basically taking away some of the benefits that pharmacies get on substituting generic product.

- Capex for FY17 should be in the range of Rs. 1,300 crores – 1,400 crores.

- Guidance for Q4 filings – well over 30 ANDAs, cumulatively for the year.

- Recent launches like Nuvigil and Vfend® generated smaller revenue but it certainly has added to the revenues over the Q2.

- $22 million is the total brand sales in US for this quarter was driven by Methergine, followed by Antara and Suprax.

- Development and approval for generic Advair – gone through a pilot study successfully and have planned the clinical trials. So if everything goes well, it will be a fiscal year 2018 filing. We are in the process of manufacturing exhibit batches and we have planned the clinical trial in the next fiscal year.

- We think the border tax overall, not only in pharmaceuticals, overall will have the impact of raising the cost of products for Americans and including drugs. So if there is a border tax on generic products, it would automatically have to be passed on to the consumers and patients and the healthcare system.

- Just finished the filing for Albuterol which has a $3 billion market size. Perrigo was the first one to file and we think there is going to be three to four players based on all of the activity that we have seen so far.

Industrials

Teamlease Services

- Average realization per associate while it is up from the comparable quarter of last year, it is down from the aspect of the start of the year and I think that an element of some renegotiations that have happened and also the volume play with certain clients that have come at a lower margin play.

- Top five, Top ten customers account for about 14% and 19% of our net revenue.

- From hiring perspective surely the demand volumes have come down but in the outsource space the demand reduction has not yet happened.

Real Estate

Technology

Havells India

- Quite satisfied with our quarterly performance amidst an uncertain and unpredictable demand environment.

- With this demonetization impact and with the GST coming in there will be a shift from the unorganized sector to the organized sector.

- Do not see an impact coming through the demand from the dealer side on reducing stocks just before GST coming because of the ambiguity on the tax rate the GST rates so that might not happen in the fourth quarter, if it is there anything it might happen in the first quarter, but hopefully by then we might have more clarity on the GST rates as well.

- Fans has been steadily growing and water heater is because of the setting up our manufacturing facility we could expand the range very quickly so there was a good traction in the water heater business appliances are also growing steadily and the new product additions of in heating in the winter season as well as the air coolers now which will start kicking in the next year, this would actually be good growing category for us.

- Nothing different at the Havells gallery store – Initially the dealers or counters, which had swipe machines or use to do a lot of business in cheques they reported better sales and peoples who are not resorting to the packages. Now things are coming back to the similar levels many of them have now installed the swipe machines anyway people are now reporting that smaller purchases have started coming back in with cash, so which is a good thing, it is a good mix today.

- We see air purifier is a very small category and a small part of our overall domestic appliances business portfolio and since we are not manufacturing this product category also we do not really focus on this as much. On Air Coolers – this is the first real year for our entry into air coolers because this is the first year when we would be selling in a major way manufactured products in our factory. This is still a small product category in the entire consumer durable business for us.

- Retailers were saying that the demand has gone down to maybe 20% levels in the first eight to 10 days of demonetization. Then they started reporting 40% to 50%. And today, I would say people are reporting anywhere between 80% to normal levels.

- No production cuts or anything of that sort entering 4Q. We are sticking to our regular production schedules.

- Capex target is still around that Rs.250 Crores to Rs.270 Crores. Already spent Rs.150 Crores, Rs.160 Crores in the first nine months – land in Karnataka for which part payment has been done, land in Rajasthan again part payment has been done. Some of the capex is left for plant and machinery as well.

Utilities

Notes:

- All figures in Rupees Crore except EPS

- NP = Net Profit After Tax

- Rev = Revenue

- EPS = Earnings Per Share (Adjusted for Bonuses and Splits)

- C = Consolidated, S = Standalone

- If we have published an incorrect data set here, do let us know.

- Where earnings go from profit to loss or vice versa, things go a little crazy with the profit and EPS growth percentages. Please ignore them.

Love it or hate it, do leave us with your reviews in the comment section below!

{kind=link}