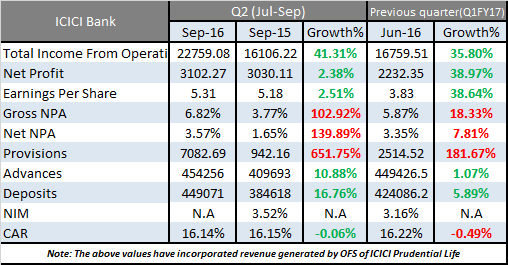

![]() When we were trying to assume the NPA issue has been slowly settling down in banking sector, ICICI results reminded us that the saga continues. The bank sees an increase to its gross NPA% from 5.87% in last quarter to 6.82% current quarter. This has for some part been expected because their “watchlist” was over 44,000 cr. last year. Around 4,500 cr. of that list has slipped into NPAs.

When we were trying to assume the NPA issue has been slowly settling down in banking sector, ICICI results reminded us that the saga continues. The bank sees an increase to its gross NPA% from 5.87% in last quarter to 6.82% current quarter. This has for some part been expected because their “watchlist” was over 44,000 cr. last year. Around 4,500 cr. of that list has slipped into NPAs.

The bank has been cutting down its corporate lending and pushing its retail division. The banks provisioning has increased almost 2 times QoQ.

The bank has showed a revenue growth of 41.31% and profit growth of 35.80% YoY. But much of that is revenue generated from stake sale in ICICI Prudential Life Insurance. If Stake sale is not included in revenue, then the revenue growth would be at mere 3.7% YoY.

The Bank has generated Rs 5129 Crs (post expenses) from offer for sale of its 12% stake in ICICI Prudential Life Insurance in the current quarter. But now it seems that, the bank hs only used all that money in provisioning of bad loans. Even in FY16 the bank sold its stake in ICICI Prudential and ICICI Lombard to generate to generate Rs 2743 Crs. This again helped as a cushion for banks provisioning scheme, which accounted for Rs 8068 Crs

Key Take Aways:

- Gross NPA growth is at 18.33% QoQ. Net NPA growth stood at 7.81%. Where as advances grew by just 1.07% QoQ.

- Advances and deposits grew by 10.88% and 16.76% YoY respectively.

- Provisioning increased almost 6 times YoY. PCR was at 57.1% for Q1FY17.

- The provision coverage ratio, despite this massive provision, is still just 59.6%. The RBI wants banks to provision 70%. An additional 10% provision means at least 2600 cr. more that needs to be provisioned, and that’s a fairly large hit for future quarters (when there will not be asset sales to protect them)

- They saw about 8,000 cr. of NPAs this quarter, of which about 4500 cr. came from the watchlist. Another 1200 cr. came from restructured loans. That means another 2300 cr. were from other sources – which is also troubling.

- Restructured loans have fallen to 6300 cr. (from 7500 cr.) and overall NPAs are 32000 cr. The “watchlist” is still about 32000 cr. more but some of it will be upgraded, such as, say, Essar group exposure.

- The bank is more protected in terms of its CAR. The stake sale in ICICI Prudential and Lombard has provided the necessary buffer.

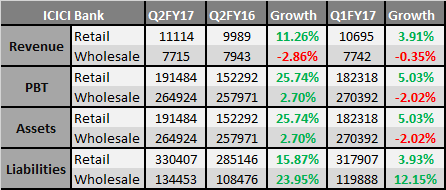

- Major revenue of the bank has been generated from its retail division compared to wholesale division. Around 48% of advances are now retail, up from 38% in 2012.

- The bank has been increasing its lending in retail sector, while cutting down its wholesale lending.

- We can see in the above table that retail deposits (liabilities) are more than retail lending (assets), and in Wholesale lending is more than Wholesale deposits. Effectively the bank uses retail deposits for corporate lending but that hasn’t worked out very well.

Results were released post market hours, the stock is up 2% at 285. The current trailing P/E is at 18.

Our View

Slippages continue to be a concern, and while the bank has moved to retail, the NPA problem can easily shift to retail too (where chances of recovery are lower). The problem, though, is that asset sale cushions will not be there in subsequent quarters. Despite taking on more provisions, the bank will need to provision between 3,000 and 10,000 cr. more over the next few quarters, which impacts profit. For that, a P/E of 17 is a bit much. The market however, seems to think otherwise. No positions at CM or with Authors.

![]()