We start a series today on what we call “Active Investing”. A multipart series on how you think about your money so you can manage it better. There is just too much bullshit on investing for the non-full-time investor, including on this site. You want a simple way to think and do. We’ll explain.

The Investing Process: Think, Plan and Do

You want to save and invest money. Largely because it’s the done thing nowadays. If you don’t have any savings, then stop here; you will just get bored. If you’re saving money, then what are you really doing?

Most people are conned by bankers into some silly insurance plan, others keep buying real estate and some will buy gold. Before going into anything further, these are just “instruments”. You haven’t even started to figure out what you’re doing yet.

Strategy versus Tactics

My ex-boss, let’s call him EH, told me one thing: Strategy matters more than tactics. More work is done thinking about what to do, than to just go do. Tactics is about choosing a fund, about buying the fund, about tracking it. Strategy is about sitting down and building out what you want from your investing life, understanding how you will get there and giving a framework to your eventual tactics.

We want to focus on strategy first.

What we think you should do is think about where you want to be. You have some idea about where you’re going, but no exactness. You have no idea exactly how things will turn out for you (will you be in India? Will you make a big bonus? Will you have huge hospital bills?). You can however make some assumptions:

- I’ll stop working at 60. Then, my savings should be enough. I won’t depend on my kids.

- I want to buy a house.

- I want to pay for my kids’ education. School and College.

- I want to pay for their marriage too. Because.

- I spend Rs. 60,000 per month today.

- Inflation, for me, is about 6% a year.

- I need something as emergency funds today in case I lose my job.

All of these can change. Buying a house is all right but not supremely important anymore. Your kids may not want your money at their marriage. You may see higher, or lower inflation. But you make these assumptions today.

The Genesis of a Financial Strategy

Now you start thinking about where you need to be. You’ve already figured out what you need.

- An Emergency Fund of 6 months expenses = 360K. 6 months is good enough. It will change as your expenses change.

- A way to save enough money to make you independent after your stop working. (Let’s call this “Retirement“)

- You want a Children’s Education Fund.

- You want a Kids’ Marriage Fund.

- You want a “Having Fun” corpus. Because we say so. Because this is what money is for. If you can’t get drunk in Italy and run through tomato infested streets in Spain and not worry about money, then you are wasting your life. And we can’t allow that.

How much do you need for each one? We’ll get there, don’t worry. We’re going to stay a little away from the specifics, because we want to encourage you to answer this yourself.

We have mentioned the concept in a previous post: Saving for retirement: How much is “Enough”?

But No, How Much?

To work out how much you need for retirement, you think of it like this:

- I spend 60K a month today.

- I retire 20 years later.

- With inflation at 6% a year, I will spend Rs. 1.92 lakh a month. This is not crazy. This is to having spend Rs. 19,000 a month in 1996, which is equivalent to your spending 60K a month today.

- That means I need to get something that brings me a cash flow of 192K a month, about 20 years later? That’s Rs. 23.09 lakh per year.

- At retirement, I think I can earn about 8%, blended, from my investments. That means if I have 1 cr. I will earn 8 lakh per year. So does this mean I need 3 crores after 20 years? No.

- After retirement, for year 1, I will spend 23.09 lakh. But then, inflation. So Year 2 after retirement I will spend 24.48 lakh due to 6% inflation and so on.

- So I need enough of a corpus to keep meeting my “increasing” needs till I reach the age of 90.

- After some trial and error, I find that the amount I need is about Rs. 5 crores – which will “finish” by the time I’m 90.

Want to learn how to use Excel for making these calculations? See our Webinar Video!

As you can see, this is a fairly simple calculation. At age 90, this assumes you’re spending Rs. 1.25 crore per year, or Rs. 10 lakh per month. Which may be impractical, but then our brain doesn’t understand compounding that well. Rs. 10 lakh after 50 years is the same as 60K, or Rs. 0.60 lakh today, at 6% inflation.

So Now, I Know Where To Go

I need to get to Rs. 5 crores in 20 years.

This is the retirement goal. Get to Rs. 5 crores in 20 years.

Let’s just say I have saved Rs. 20 lakh so far, till age 40. This is all I have. How do I get to 5 crores?

It’s not unachievable.

Now, We Get To The “Achievable” Return

We still aren’t talking which mutual fund or which stock. We don’t care right now. Remember, it’s the process. We know where to go. We just need to get to Rs. 5 cr in 20 years. We can get there by anything – stocks, mutual funds, real estate etc.

Then, we look carefully. We have 20 lakh. We need to get to 5 crore.

If you do your standard calculation, then you need 17.5% per year for 20 lakh to become 5 crores in 20 years. Possible?

Sure! In the last twenty years we saw a growth of approximately 10x on the Nifty (12%), and one fund which launched in 1995 – Reliance Growth Fund – has returned 90x in about the same time, which is 25%. (Again, a big win for active investing, but we digress)

But the next twenty years are not going to be the same. The last 10 years weren’t the same. We saw the Nifty only go up about 9.5% per year from 2006 to 2016. That same fund – Reliance Growth – went up about 14.7% per year.

Betting on 17% is fraught with danger – it’s too much risk and a very low chance of a great return.

But at the same time, your “risk free” rate is around 7% today. That’s what you can get in the lowest risk instruments around, especially if you look at the 20 year government bond (2036 maturity).

So 7% is the minimum. 17% is a tad high on risk, perhaps. SO what do you do? You can then choose a number in between, or 12%, for a reasonable return.

For an investor, getting 12% is a good deal. It’s 5% greater than the risk free return on a 20 year period, and it’s not so high that you can’t achieve it.

Now I Know Where To Go, And How Much Return I Can Expect

I need to go from 20 lakh to 5 crores. I estimate I can get 12% a year. This is a good start.

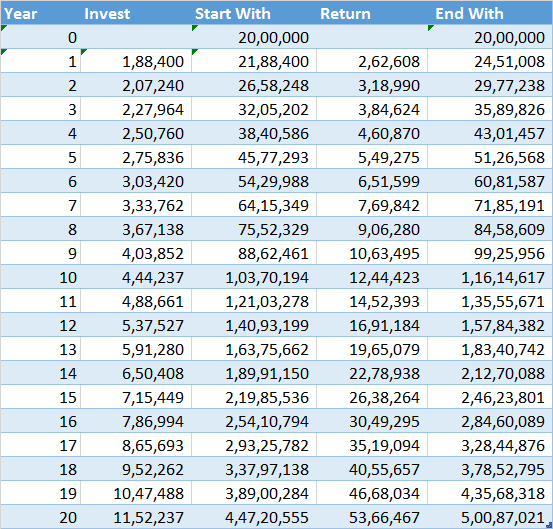

Now, you work the numbers. 20 lakh alone, in 20 years, will only grow to Rs. 1.92 crores at the 12% return. How do you get the rest?

The answer: You Invest Every Month.

How much? Look, in 20 years, your income will increase. So you can increase the amount you invest. Let’s say you can increase it by 10% every year. Calculating backwards, here’s how you get there: You invest Rs. 15,700 per month in year 1. Then you increase this amount every year; in Year 2 it’s 17,270 per month. In Year 3, around 19,000 per month and so on. Here’s how you get there – with returns of 12% per month on that plus your initial capital of Rs. 20 lakh.

Want to learn how to use Excel for making these calculations? See our Webinar Video!

And This, Dear Reader, Is Your Financial Strategy for Retirement

See, you got there by just some calculations:

- You invest 20 lakh today

- You attempt to get 12% returns

- You will add Rs. 15700 per month

- This amount increases by 10% every year

- And when you’re 60 (20 years later) you will have Rs. 500 lakh (5 crore).

- This money, at 8% a year, will last you till you’re 90, assuming inflation is at 6% and your expenses are the equivalent of 60K today.

That’s it. Finished. Now, you have to get down and do it. Now for the tactics.

In subsequent parts in this series, we will speak of building your own plan in a larger way, thinking of other goals you can properly define, and how to map your progress.

The Tactics: Where To Go and What To Do?

Only after all this do you say: Now what do I buy?

Why does everyone say “Invest in stocks”, or “Buy mutual funds”? Because you apparently get a higher return when you do.

This is pointless. You want 12% a year. That’s about it. You don’t want supersized returns. All they will do is make you take more risk. If you get an 18% return, it’s great, but since you expect 12% in the longer term, you can then slow down; further money can be put only in “safe” instruments, waiting for the market to bring your “average” return down to 12%. Either the market will fall – which allows you to reinvest whatever you didn’t invest, at lower valuations – or you will find that you’re automatically diversifying into part-equity, part-debt.

Let us plant the seed of an idea into your head.

How much “more” have equity markets returned compared to risk free returns?

The “Equity Premium” – Higher Return for the Higher Risk

Liquid funds don’t fall in NAV. (Okay maybe at extremes but they mostly don’t). Equities fall all the time. You may require money when they have fallen. Which is the risk you take.

You expect to get a higher return for that risk. In India there has really been ONE period when that risk has been adequately compensated, and that period was 2004 to 2008 or so. Let’s demonstrate.

We take an “SIP” into a liquid fund (a systematic monthly investment, or a Systematic Investment Plan) which is the safest instrument around. Then we compare that with an SIP into the Nifty index, with dividends reinvested. (We use a “Nifty TRI” index for this purpose, whose data is available since 1999).

Take a 3 year SIP and see the rolling returns over time for each component. Rs. 10,000 bought every month into either investment, shows us the “easy” earning (liquid funds) versus the risk (Nifty). The compounded return differential between the two is the “Equity Risk Premium”.

Now if you can get 6% risk free, you should be able to 12% when you have risk. The difference between “risk free” and “with risk” is the premium the market is giving you for taking this risk. That premium has changed over the years. In India, a 10% risk premium is awesome. Ignore the early years, but over time you can see that the Equity Risk Premium goes up very heavily and then comes back down to nearly equal to the risk-free SIP, and then goes back up.

You can see here that even at a three year level we haven’t really lost too much money compared to a liquid fund. We may, of course, see this change in the future.

But it also tells you this: if you’re seeing a risk premium close to 10% or more – at least in the last 7 years or so – you are likely to see the market fall and correct this premium over a short time.

One way you can build your tactics is that you will keep a higher allocation to equity, in general, when the Equity Risk Premium is lower than +10%. Above that, you’re going to not invest further in equity.

This means a tactical plan is like this:

- I invest in a blend of equity and debt for my retirement.

- I want about 12% per year

- I know – from the excel sheet above – how much I need to be at every single month from now.

- I need to find investments that yield me 12% a year

- I start with 50% in debt funds – a “Dynamic bond” fund sounds useful when interest rates are falling. I might split this amount into some “Liquid” funds and the rest in bond funds.

- The other 50% goes to an equity diversified mutual fund, or direct equities or such.

- Every month I invest Rs. 15,500 in a similar proportion – half debt and half equity.

- If the Equity Risk Premium crosses 10% I put no money into equity.

- I check at the end of the month : am I where I’m supposed to be? (See third point above) That involves adding up all the investments and seeing the total current value. If I’m Rs. 3000 short, I will invest Rs. 3,000 more next month.

- If I’m at where I need to be, or higher, I will not invest – I’ll just put the money into a liquid fund. Then I can use that money when I fall short at a later date.

- Every year I increase my monthly investment by 10%.

- In 20 years, I’ve cruised to my goal. I can change the assumptions, I can change the amounts – all it does is gives me new numbers for each month going forward. My tactics are all built to reach my goals.

You can’t be exact – you need to leave lots of buffers. But the main point is this: Investing actively, according to us, is to take control of your future and to target your goals. Without that, you just blindly invest without knowing whether it’s enough, it’s going well, or it’s worth your while.

Your financial strategy is more important than the tactics. Notice how we didn’t say “which fund” or “which stock”. All that is tactical and can change. Even taxes are tactical – your tax arrangement in one year will determine what you invest in – but the strategy remains the same: Get the 12%, Invest X every month, Match yourself to your goals.

More coming up in immediate posts. Tell us what you think.

Read the Other Posts:

- Feedback and Q&A on Part 1: Taxes, Allocations and more.

- Part 2: Using Covered Calls To Reduce Cost, and Generate Business Income.

- Webinar: How To Hedge Your Portfolio

The first part of this series is open for non-premium investors, and some subsequent articles may only be for Premium members. Subscribe now!

Want to learn how to use Excel for making these calculations? See our Webinar Video!