Beat FD returns with Bonds

If you bought a stock, would you think a bond from the same company is, somehow, in trouble? There are a truckload of corporate bonds that are listed on the exchanges and because of how complex they sound, they are shunned by investors. But it’s surprising that while people are willing to buy a stock – at any price – the bonds of the same company sometimes quote like they are going to fall off a cliff soon.

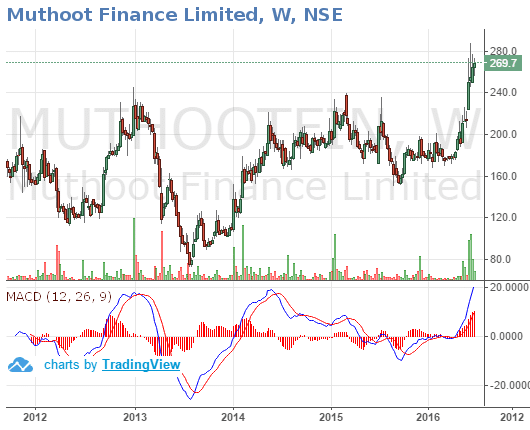

Look at Muthoot. It’s a company that finances gold purchases. It’s been around for a long time and the stock has recently gone back up after the big gold fiascos that have been happening recently.

And yet, the bonds of this company, whose stock has now gone up 50% from the lows of last year, trade almost like the company has a high likelihood of defaulting by September.

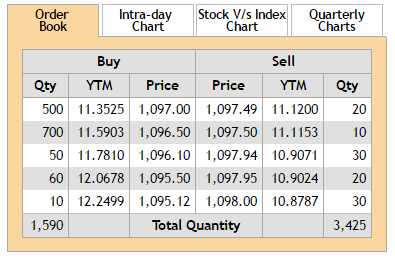

One of its bonds, the Muthoot N6 bond, is trading at 10.4% yields!

These NSE Yields are just wrong.

Why?

- Because this bond is simple. You buy it today, it gives you Rs. 1000+12.25% interest = Rs. 1122.50. When? On September 14, 2016.

- To calculate the yield you would simply say I’m going to buy it at some price – the best sell price is Rs. 1097.49.

- And in a few months, on September 13, they will pay me Rs. 1122.50.

- The interest rate is simple: 2.27%. But this is only for today (23 Jun) till September 14.

- Which is 83 days. If you work it out, the yield for 365 days, the yield is 10.41%.

30% better than an FD?

- A three month fixed deposit from most banks is less than 7.5%.

- Take a Rs. 500,000 rupee investment. If you put it at 10.41% a year – for 83 days – you will make Rs. 11,800 as interest. If you put it in a bank at 7.5%, you will make Rs. 8527.

- The former is better by over 38%!

- But, you will say, look boss, it’s far more risky!

- I understand that this makes sense if you are looking at a longer term. For a 5 year, or even a 1 year term, you will have to account for the higher riskiness of a Muthoot, compared to say a State Bank of India. But for 83 days? Do you think Muthoot will keel up and die in 83 days? If so, wouldn’t the stock price reflect it by showing a trend downwards rather than the nice little upward move we are seeing?

Forget it Bond Baba, I Will Listen To Rating Agencies Only

Ok. But while I cannot trust a rating agency for what it says, I understand you want to.

Rating agencies actually have two kinds of ratings. One is for long term debt, and one is for short term. Because they know that while a company may be shaky in the longer term, the short term may have more visibility.

ICRA, which rates Muthoot’s debt, gives it a rating of AA- in the long term. (Read Feb 2016 rating) But in the same document it mentions that:

ICRA has an outstanding rating of [ICRA]AA- (stable) to the various Non Convertible Debenture, Subordinate debt programme of the company. ICRA also has a rating outstanding of [ICRA] A1+ to the short term fund based limits and Commercial Paper programme of the company

And what’s A1+? It’s the highest rating ICRA has. In the long term, the AA- means about six notches below the top (AAA+ being the top). But A1+, for a short term instrument, is the top rating available.

Basically ICRA feels that Muthoot could be a riskier bet in the long term, but the short term default risk is very very low.

Bond baba doesn’t say it. ICRA does.

83 days is short-term. So if rating agencies are your superheroes, then this bond – maturing in 83 days and therefore, short term in nature – is as close to top class as you can get.

But Of Course There Are Risks

Rating agencies don’t generally know enough. So yes, there is a risk. Muthoot could go under. This bond could be “unsecured” and therefore, after a default, the company might have to pay others (banks, secured lenders) before it paid you. So it’s got that much larger risk in the case it does default.

Bond Baba believes that there are risks but sometimes the reward is better than the risk. While we can’t keep telling you to buy bonds of anything and everything, this particular case is peculiarly rewarding: an 83-day bond of a company that continues to have an A1+ rating and where the stock price is just going up, and yields 38% higher than an equivalent fixed deposit.

The negatives? If things start going bad after you buy, you may not be able to sell these bonds. And then if the company defaults, you have a problem. The other negative is that you don’t really know if you get the money on the 14th of September. What if there is a big delay at the registrar end and you get the money after one week? Your yield falls to 9.56% which is far lower than you started.

These risks remain, but is a 10%+ return worth the risk? Remember, a 10.41% in the 30% tax bracket (30.9%) is still about 7.2% post tax, and that is higher than most tax-free bonds today. Yields there are 6.75%.

Wait, Can I Get A Higher Yield?

Of course you can. Prices change everyday, and a higher yield has been seen in other bonds. A few months ago, Shriram Transport Finance bonds were trading at 12%+. Other bonds include Manappuram Finance, IIFL Finance, ECL Finance, State Bank of India bonds (which have better yields than SBI’s own fixed deposits) and many others.

Getting a higher yield is about tracking all these bonds and figuring out which bonds work in terms of risk/reward.

Pain Points

We know that:

- There is some risk of the company defaulting. You can never say it’s zero.

- Liquidity is an issue. Putting Rs. 500,000 on this bond and still getting that yield is going to take some work on the terminal.

- There is some risk of delayed payment due to procedure.

And The Gyan

You are a better person when you know what you did, or did not. Most of us are blissfully unaware of these kind of bonds, and the yields they bring to us. Bond Baba will help, and you will see a lot more information in the coming days. This bond above may not have a great price tomorrow – and if enough people follow the Baba, the yield may fall below 10%. At which time even Baba would not buy this bond. But at 10.4% or higher, this could be a reasonab

ly rewarding purchase.

ly rewarding purchase.

In the next edition we will tell you about an incredible one month opportunity in another bond. But till then we leave you to do your homework: Find it.

We are not the kind of baba that says, don’t think of the reward, just take the risk. If an Ekalavya cut off his thumb for Guru Dakshina, we will first attempt to get a hospital to sew it back and then give him a scolding he will never forget. There is nothing for Bond Baba in sacrifices or Russian roulette. Respond to your brain, not your adrenalin. Take a risk when there is an adequate reward.

More on bonds and mutual funds is available at #bonds-and-funds on our Slack, which is available to all Capitalmind Premium members. If you’re not already subscribed, use discount code GETCM for a 20% discount, valid through June 2016. Our plans start at ₹1,333/mo (post discount).

Disclaimer

Please do not treat anything in this email or at Capitalmind Premium as investment advice. Capitalmind Premium does not provide any recommendations of securities. However, you may choose to consider our content as one input in your decision making process. While we may talk about strategies or positions in the market, our intent is solely to showcase effective risk-management in dealing with financial instruments. This is purely an information service and any trading done on the basis of this information is at your own, sole risk. “Bond Baba” icon created by Rohit Arun Rao from Noun Project.