What if we told you that there is a way for you to:

• Make part of the Nifty gains on the upside

• Be Fully Protected even if the Nifty went down by half.

This protection is available for a portfolio of Rs. 600,000 (or a multiple of it)

Here’s the method, for a portfolio of Rs. 600,000.

[level-capmind-pro]

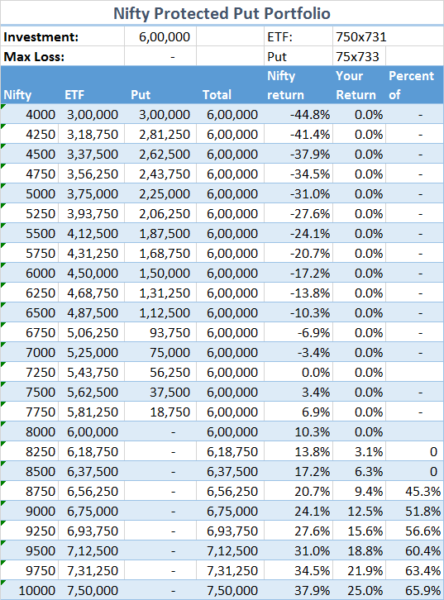

1) You buy the Nifty ETF (Nifty BEES) – where one share is equal to Rs. each of this trades about 731 now. You have to buy 750 quantity. This adds up to Rs. 548,250.

2) You buy a December 2016 8000 put at Rs. 733. One lot is 75, so you pay around Rs. 55,000.

The total amount invested is about Rs. 603,000 (which is slightly higher than the 600K required but stay with us).

How Does This Protect You?

Let’s look at things in a “binary” way. You’re going to do this and forget about it. No coming back before December.

If the market has fallen, let’s say, to 6000 on the Nifty, here’s what will happen.

1) Your Nifty ETF will be at Rs. 600. So you can sell it and receive Rs. 450,000 from it. Bad? Wait.

2) The put will pay you: Since the strike price is 8000 and the Nifty is at 6,000, you get the difference = Rs. 2000 per Nifty. One lot is 75 Nifty so you make 75 x 2000 = Rs. 150,000

3) The total return is Rs. 600,000 (450K plus 150K).

Meaning, your principal is fully protected. No matter how much further down you go, you will lose on the ETF and gain on the put.

What about the upside?

Say Nifty reaches that awesome 10,000 level in December. From the current level of Rs. 7250, that’s a 38% return!

That’s brilliant no? Can we get some of it? But wait, haven’t we lost all that money in the put? Let’s see:

1) The ETF trades at 1000, so you get Rs. 750,000 for the ETF position.

2) The put expires worthless, since the Nifty is above 8000. So Zero.

3) Your investment was Rs. 600K, now you have 750K, so you have made about 25%.

While the Nifty made 38%, you made 25% which is a reasonable return on the upside.

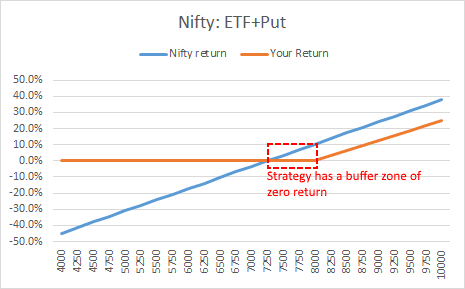

The Payoff Graph

As you can see the strategy protects the downside to the full – there is, literally no downside.

Note that there is a portion of “zero” return – here, it means that you make no returns until Nifty is above 8000. Meaning, from 7250 (current level) to 8000 in December, this ETF+Put portfolio makes nothing. Above 8000, it starts to track the Nifty. This is the zero return buffer.

We Paid 3K Extra!

If you’re wondering why we calculated returns on 600K when we actually made 603K in investment – the answer is: The Nifty ETF (NiftyBEES) should have traded at 725, as it’s 1/10th the value of the Nifty.

But it’s at 731, why?

Because the ETF includes the value of dividends, which has added about Rs. 6 to the value of the ETF. That Rs. 6 will be available to you later (and might actually go up as dividends get paid in June to September) and that “extra” will make up for the 3K extra you paid while getting in.

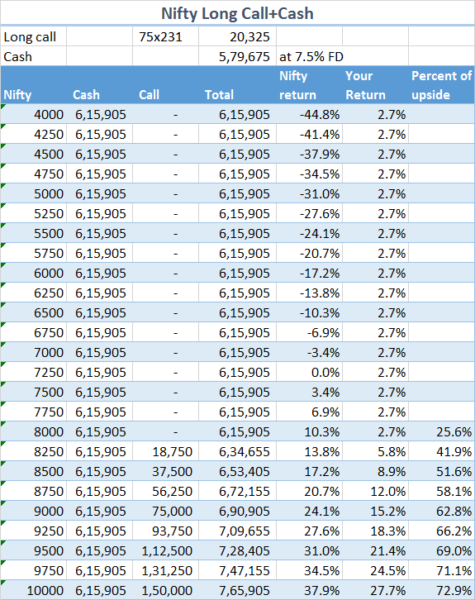

Or: Can’t We Just Buy A Call?

The payoff diagram looks just like a long call option. That’s because a long stock (ETF) + long put is equivalent to a long call!

Why don’t we just buy the 7500 December call instead? And put the remaining money into a fixed deposit at 7.5% for 10 months?

The pay off is juicy:

In fact, here, we make a better percentage of upside no matter where the Nifty goes, and there’s only one transaction to worry about.

When to use one or the other?

You would use the put if you already had a position in stocks, as a buffer against a future fall. Now doing the 8000 put (December) is expensive, but provides a zero downside. You can reduce the cost further by using a 7500 put (Rs. 470) or a 7000 put (Rs. 300). The above numbers limit your losses to -3.6% and -8% respectively, but give you a greater percentage of the upside.

You would use the cash+call if you had no positions right now, and wanted to build a position that gave you no downside but the full upside.

Why Isn’t Everyone Doing This?

If it’s so good, why isn’t everyone building a portfolio like this? For one, there isn’t that much of an appetite for Futures and Options. And then, there’s the tax mess of having to report the income on puts or calls as business income. (The good part is that you can offset some of your expenses with business income, if you don’t already have business income.)

For another, this strategy isn’t very exciting. It’s one that is designed to “underperform” the index on the upside, but give you complete downside protection.

But excitement is for casinos and entertainment! What you want really is downside protection and you don’t mind giving up a part of your upside for that. This is what people actually do by diversifying between fixed deposits and market investments!

The Absolute Return Portfolio

This kind of strategy focusses on absolute returns – not something that loses less money when the market falls (which would be a “relative” return) but something that doesn’t hurt if Nifty falls, but does reasonably well if Nifty goes up.

If you’re looking for a blended return of about 10% and you believe you get 8% in Fixed income and 12% in stocks, this might just be a useful mechanism for obtaining that return. Would you like this kind of portfolio as and when there are visible opportunities? Please let us know, we would love to create a product that identifies such opportunities and presents them on the Snap platform.

And there are other options you could take:

• A December call option at 480 at the 7500 strike – this gives you a smaller “zero return” buffer.

• Go even longer term: the 8500 December 2018 call has some liquidity which gives you a three year protection.

Fund managers of structured products usually charge 2% to 3% for such a structure; at Capital Mind, it’s just another part of your subscription!

Note: We have done this before:

1) In November 2013, we proposed three different ways to make downside protected portfolios.

2) We revisited these portfolios in mid 2014 and end-2014 – we had a fully protected portfolio (for a downmove) and made a reasonable return on the upside.

Do connect in the slack channel or reply to this email with your comments!

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

[/level-capmind-pro]