In the Budget, we asked the question: Is a 30,000 cr. debt switch planned for March? Of course it was, it turns out.

The government was looking to switch debt worth 30,000 cr. from an immediate repayment (FY 2016) to a later year. And here’s why:

[fusion_lightbox]

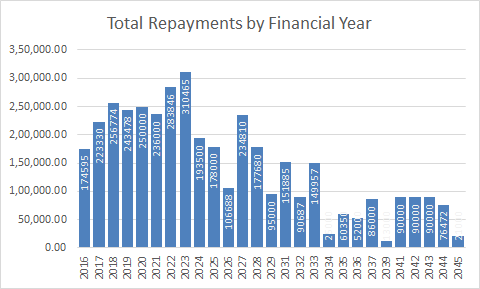

Government Debt maturity by Financial Year

[/fusion_lightbox]

On Friday the RBI switched out 30,228 cr. worth securities from the FY 2016 to Fy 2027. This means the government effectively bought back securities worth Rs. 30,228 cr. maturing FY 2016, and issued new securities maturing FY 2027 in exchange.

Whatever is repaid has to be re-borrowed because our governments are big ponzi-type schemes – debt can only be paid by issuing more debt. So a “shuffle” in maturity patterns can lead to smoother redemptions and reissues; essentially the government will need to reissue 30,000 cr. lesser of new bonds because of this swap.

But what’s the big deal? Even last year, the government switched out Rs. 31,000 cr. worth debt securities.

There’s a big difference. Last year, the RBI acted like a merchant banker, and did the debt swap with external institutions. Companies like LIC, or pension funds, would own near term bonds, and would want to buy longer term bonds – they will happily exchange these securities so that they can get a hold of a large chunk of longer term bonds locked in.

This time, the RBI did it with its own securities. Meaning, instead of finding a third party that owned recently maturing debt and offering the longer term securities, RBI hunted inside its own books, and exchanged securities maturing in the near term to new securities issued that will mature FY 2027.

What is the significance?

Well, RBI is not supposed to directly buy debt issued by the government. That is equivalent to financing a deficit by printing money. Even in the US, the Fed buys securities from the market, while market players buy bonds issued by the government. This may sound like a useless step in between, but in India’s case, the history has been that RBI has monetized our deficit earlier, and therefore the extra precaution of never allowing it to directly buy bonds of the government.

We wonder why the RBI did this instead of swapping the securities in the market with a different institution instead. Were there no takers? Did the pricing of the deal happen at a number very favourable to the government? Why didn’t they publish the prices at which they swapped the debt, since these questions would obviously have come up? This is why you need a public debt management office, instead of the RBI managing such transactions; there should be no conflict of interest.

If you’re interested, the specific securities that have been switched are:

Government buys back:

- 19,500 cr. of the 7.17% 2015 bond, maturing 14-Jun 2015. (New Outstanding: 33071 cr.)

- 10,729 cr. of the 7.38% 2015 bond, maturing 3-Sep 2015. (New Outstanding: 45,649 cr.)

This reduces the redemptions in FY 2016 to 144,366 cr. (down 30,228 cr. from earlier)

The government also issued about 29,067 cr. worth bonds of the 8.15% 2026 bond maturing 24-Nov 2026. (This is Financial Year 2027)

![]()

Subscribe to Capital Mind:

To subscribe to new posts by email, once a day, delivered to your Inbox:

[wysija_form id=”1″]

Also, do check out Capital Mind Premium, where we provide high

quality analysis on macro, fixed income and stocks. Also see our

portfolio which has given stellar returns in our year, trade by trade

as we progress. Take a 30-day trial:

[wysija_form id=”2″]