Mutual Funds have been in vogue as an investment class ever since their introduction in the 1960s with UTI introducing the first Mutual Fund in India. It has undergone a sea of changes and upgrades since those days, with public sector banks and other NBFCs throwing their hat in the ring as the years went by. The first private sector funds were set up in 1993, and this coincided with greater awareness among the general public about investing in Mutual Funds.

Currently, there are more than 40 AMCs in India that offer 1000+ MF schemes. Mutual Funds are currently offered in 2 forms – Direct Plan and the Regular Plan. This was based on how a customer invested in the Fund, either directly or through a distributor. This segregation, or rather the additional choice that the investor community was given, surfaced only in Jan 2013. Up until then, an investor would compulsorily have to approach a distributor in order to invest in a scheme, thereby indirectly paying commission fees to the distributor. However, SEBI brought in new regulations in September 2012 by way of which schemes would have to be made available to investors who wanted to bypass the middleman. As customers got more and more financially savvy and aware, the opportunity for the more technically sound ones to invest directly in a MF without the middleman sprang up in January 2013.

For obvious reasons, investing directly in a MF scheme would yield better results. Take away the middleman, and you now have one less person eating away at your share of profits. But investing in Direct Plans does come with its own caveats:

- A lot more paperwork to be filled in before investing, which is taken care of by distributors.

- Direct Plans require a substantial prior knowledge on MFs; distributors generally provide comparisons and a wide range of choices if you go through them.

Bottom-line: Way more research work and diligence is needed if one opts for Direct Plans. But how much reward does one get for choosing to do the dirty work oneself? That is what we look at below.

The AMFI website is a terrific place to obtain all sorts of data related to MFs, from AUMs to NAVs to monthly newsletters about the space and so on.

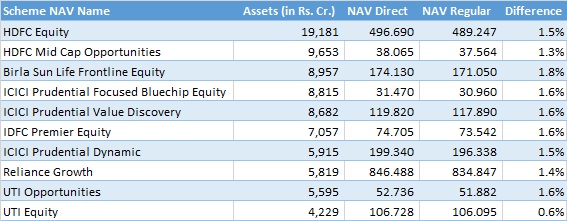

We picked out some of the top 10 funds based on AUM and list them out to see how much extra return can be obtained by going Direct.

On an average, these funds would have given you 1.5% extra, had you invested directly in them. These additional returns are over 2 years, starting January 2013 when the Fund houses made this approach available.

That is, effectively the return of a “Direct” plan is better by 0.7% per year. That is the “cost” of your distributor.

Note: Buying from a Bank, such as HDFC Bank, means you are using a distributor. Even if you buy an HDFC Mutual Fund, HDFC Bank acts as a distributor. We know this is confusing, but that’s how it is. The only way to buy “Direct” is to have “Direct” in the fund scheme name – if the scheme doesn’t say “Direct” in your report, you are paying commissions.

The portfolios of both Direct and Regular plans are exactly the same. Yet, the Direct plan makes better returns, by 0.7% per year!

For clarity: If one were to make an investment in let’s say, Reliance Growth Fund, the higher return of the Direct Plan would mean that for the same amount of capital, your return would be higher than the return you get if you invested in the Regular plan.

We have a more substantial list of 291 such schemes with the differential returns on a Google Spreadsheet which you can access.

In Part 2 of this post, we will show you how investing in direct plans make a difference, versus regular plans, and what you need to do to benefit.

![]()

Subscribe to Capital Mind:

To subscribe to new posts by email, once a day, delivered to your Inbox:

[wysija_form id=”1″]

Also, do check out Capital Mind Premium, where we provide high

quality analysis on macro, fixed income and stocks. Also see our

portfolio which has given stellar returns in our year, trade by trade

as we progress. Take a 30-day trial:

[wysija_form id=”2″]