Recently, an article in Business Standard claimed that based on their sources, GTL Infrastructure had apparently defaulted on their loans.

“More than a dozen banks are now staring at Rs 6,000 crore of fresh non-performing assets, as GTL Infrastructure, a Mumbai-based company in the business of shared passive telecom infrastructure in the country, has failed to repay its restructured loans. Sources claimed Indian Overseas Bank, one of the lenders to GTL Infra, had already classified its advances to the firm as NPA; other lenders were expected to follow suit.”

(P.S. We cannot find this article anymore. It may have been removed based on the clarification provided below by GTL Infra).

After BS reported their story, GTL Infra clarified with the BSE on their side of the story, vehemently denying that they defaulted.

“Your statement that GTL Infrastructure is an NPA of Rs.6,000 cr. is baseless… as on September 30 2014, total out-standing debt is Rs. 3,432 crores…. GTL Infra Limited has paid Rs. 681 cr. to Banks… is neither in default nor classified as NPAs.”

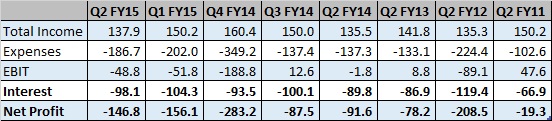

Here’s a snap-shot of GTL’s recently released Q2 FY 15 earnings, along with some comparisons with previous quarters:

All figures are in Rs. Cr.

On November 8 2012, GTL Infra successfully obtained shareholder consent in order to go into a Corporate Debt Restructuring (CDR) program.

From the data, we can see that each quarter, the company has been paying a hefty amount as interest charges. ). As per their statement, GTL Infra claims to have Rs. 3,423 cr. as outstanding loans under the restructuring mechanism.

Update: Alert reader Siva points out that the Rs. 100 cr. per quarter being paid is just interest. We don’t know how much principal is being repaid. But, it’s evident that interest costs have been more than 50% of their REVENUE (before costs of running the company), as long back as Sep 2011. Even Profit before Interest is negative, meaning there’s hardly any scope to pay back the principal part of their loans.

It appears they got a two year moratorium on debt repayment in 2011, which would have matured now. With sustained losses, the company will need to keep borrowing more, or raise equity, both of which look increasingly bleak with the restructure in progress and the share price in the doldrums.

The stock peaked at 100 in 2008, and was still at Rs. 50 in 2010. It has now fallen to Rs. 2.75.

Our View:

For a company that has been consistently reporting net losses, without any substantial increases in revenues, it is indeed hard to fathom how they will continue to repay their loans. We are not privy to the terms of the CDR agreement, hence we cannot say if asset sales or plans of raising additional equity are in the frame. Again, with such heavy debt burdens on the balance sheet, and at such a low share price, will raising additional equity be a viable option?

One piece of good news was the agreement signed between GTL Infra and Reliance Jio for tower sharing. This should increase their revenues. But by how much? And will they be able to sustain such measures in the long-run? (Remember, Rs. 3,243 cr. is still outstanding). We will wait and see how this story unfolds.