This is a premium post for Capital Mind Premium subscribers.

How do you setup option positions for elections? We saw this question in the premium group today and we were hoping to expand on certain option strategies; here we go!

[level-capmind-pro]

We’re going to take the political position of “Oh, we don’t know what will happen”. Which means we have to evaluate What-Ifs.

Let’s take three situations:

- Modi-fied: BJP and allies get 240+ and can easily cobble together a majority of 272. Economic policies and reforms not under stress.

- Shifty Eyes: BJP etc. get less than 240, AAP gets a lot of seats and basically it will need parties to really collaborate to get a majority. Possible dilution of economic agenda.

- Whoa: Any other scenario like a Congress based Majority, the Left playing a part etc.

What we expect is that in case we’re Modi-fied, markets will go up, and in the other two cases, the market sees a 15% down move within a few days. Largely because we’ve run up recently. However the probability of the first is very high at the moment, so let’s not bet on the “falling down” bit just yet.

The election results will impact markets.

For multiple reasons:

- There’s been a lack of solid decision making by the government. They have stalled projects and created fear in the minds of direct investors who have borrowed money but have to wait for clearances before things get done. Elections with a solid government, people feel, will change things.

- The corruption situation: People believe that the current government shields the corrupt, and that a new government will reduce this friction to investment.

- Reforms and liberalization will continue with a new government.

The lack of a solid new government will obviously break this thinking. Volatility, therefore is the order of the day, especially if we are in “Shifty Eyes” or “Whoa”.

What happened in the last few elections?

- 2009: Markets shot up 20% in a massive up day, the first up-circuit ever after it was evident the Left would not be part of the government with their dismal election performance.

- 2004: The NDA alliance lost, after what was five years of apparently good performance, and the Left was needed to help create the Congress government. Markets crashed 10% but recovered in a few months.

- 1999: The NDA came to power, after losing its earlier position by a single vote! This time they got 270 seats and a clear majority. The Nifty, however, moved from 1378 on 5 October to 1470 on 7th October, a quick 6.6% move up. However that fizzled very soon, as markets closed at 1325 for the month.

- 1998: Counting was in March 1998, and the BJP/NDA came to power on a thin margin, needing the AIADMK to support them. Markets however were not responsive to the election result, up only 1.5%. However, they ended the month up 5%.

Given the sheer lack of enough data points it is very dangerous to assume that markets will only go up or down big time on elections. Plus, remember that markets were not that big in 2004, and futures and options weren’t as liquid at the time, so we don’t have enough derivatives information to conclude much.

However, considering the fact that this time, it’s a tough and go for the economy, we’ll see markets react appropriately. So, what positions can we take to benefit from market moves?

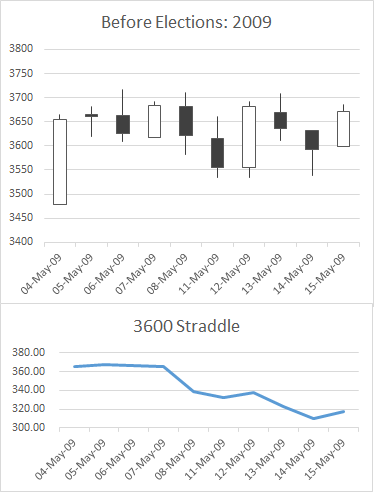

Let’s look at 2009

Worldwide, markets bottomed in March 2009. Then the markets took a turn for the better, and in India, they went up nearly 30% before election results were due in May. There were low expectations – after all, there was a disaster in the last year, inflation went to very high numbers, the world crashed down, the economy was stagnant and so on.

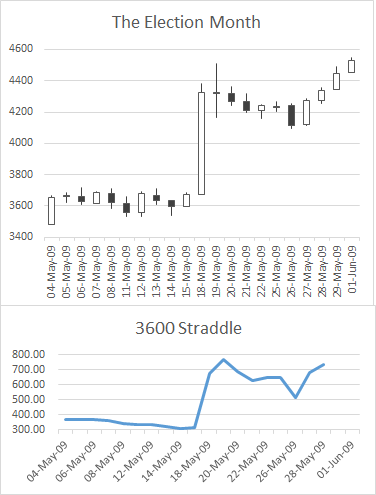

However, voters chose the Congress by a number that wouldn’t require the support of the Left parties, which took the market up by over 15% in one single day (and required markets to be shut because of circuit limits).

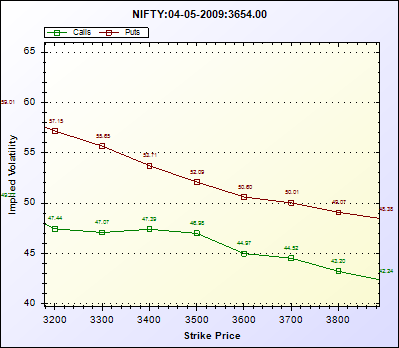

Options data for a few days before elections showed markets expecting moves of over 10%, with the 3600 straddle at Rs. 320 on the friday before the results (which came out on Sunday).

However, what happened afterwards was a blowout.

This was crazy but it was happening. The markets simply did not predict the volatility, despite the obviously large stakes.

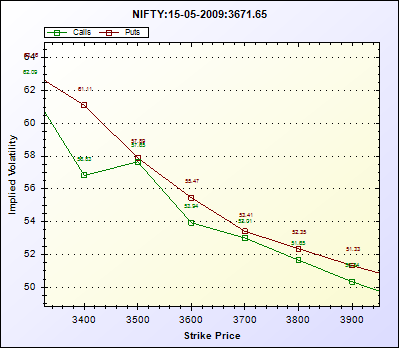

The 3600 straddle at that time was quoting at a very high implied volatility at the time, even though this data has been calculated at current risk-free interest rates of 10%. The call and put IVs went up towards elections, calls going up more than puts.

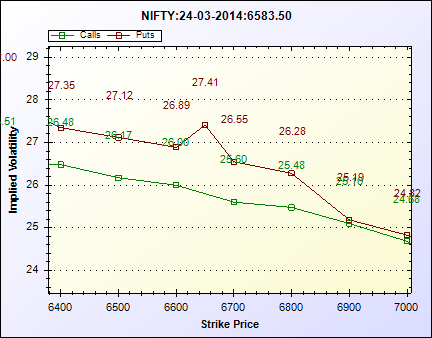

Let’s look at the IV situation today. For the May 2014 expiry, we have some traded information and here’s where we are with respect to Implied Volatilities.

This is very low, but that’s not the real point.

(Note: this is a test tool we have developed to calculate IVs for any date. We will soon make this available to all subscribers!)

As you can see, IVs of puts are still higher, however both still are low for a massive upmove. (10% in a day is much greater than the 2% a month expected)

Option Strategies To Use

We will cover some of these in the webinar later this week. One of the simplest ways to trade options for this event is to buy a straddle. Our only data point shows success (the 3600 straddle doubled!), but one swallow does not make a summer. A Straddle today costs around Rs. 600, which is a 10% move likelihood over the next two months.

To find out how much a straddle costs, check this page, which has data for all calls on the left and puts on the right. Just add the “LTP” – or last traded price – numbers for the strike price closest to the current market price. Remember to change the expiry date to May 2014.

A straddle will only benefit if the Index moves 10% in this much time. But that’s just to break even! This is not very profitable unless you have a very large move.

Could we go short a straddle? The reward is likely to be larger here, as a straddle will converge to lower values. However, this strategy has unlimited risk and we need to limit that risk. The same applies with strangles (where the strike prices are different).

The Condor

Let’s consider a Condor. The strateg

y is a combination of a long strangle and even wider short strangle. Consider the following positions with May 2014 options:

- Buy a May 2014 6300 put for 146

- Sell a May 2014 6000 put for 84

- Buy a May 2014 6700 call for 294

- Sell a May 2014 7000 call for 163

(Assuming quantity of 100 shares of Nifty for all legs.)

For 100 shares, you will pay Rs. 193 (294+146-84-163) each or a net debit of Rs. 19,300. Additionally you will need margin of around Rs. 30,000 for the position.

This has a payoff that loses you money unless the Nifty moves big time. Like you see:

It simply doesn’t make sense to do this in normal times, but in a large event if you expect a 10% move, you could build this strategy. You lose upto Rs. 20,000. You make only Rs. 10,000 for a win. But the idea is that it’s more probably you will see a big move, so it makes up.

Such a strategy is a defined max risk and defined max reward situation; and is probably better built later in April to avoid the time value destruction.

This is called a Condor because the payoff sorta looks like one.

However the range of operation is wide. Profits are only less than 6100 or higher than 6900.

The Butterfly

Assume the following positions

- Sell a 6300 call at Rs. 540

- Buy TWO 6300 calls at 345 (At the money)

- Sell a 6900 call for Rs. 200

(Assume a call = 50 Nifty)

For 50 Nifty you will receive premium of (-540+2×345-200) = Rs. 50 per share, or Rs. 2,500 total.

This results in:

As you can see, the max loss is higher, but we can work with a narrower band (6350 to 6850) This position benefits from a large move, but how much?

The max profit is Rs. 2500 for all that effort, and you’ll need to put in about Rs. 40,000 as margin. The max loss is Rs. 12,500. This is more risky but there is a very large chance the Nifty closes very differently from 6600 in March.

Which one should we take?

We should wait till April 1. That’s when RBI releases its Credit Policy and Options could change based on that data. We don’t expect any fireworks, or the chances of actually announcing big things because of election rules. However, the volatility premiums currently contain the element of risk of a big move due to an RBI action, and we need to eliminate that while trading in for elections.

We can get to similar positions in other indexes, especially the Bank Nifty. In stocks we should be careful in only taking such positions with ultra-volatile stocks, but at the same time the butterfly or condor should make sense in terms of risk/reward.

Other events next month involve results – nearly every stock will announce results before elections and option positions like butterflies might still work, even earlier than the expected end-date.

A Recap on Options.

Notes on the earlier moves: We bought a very small quantity of the 6500 straddle and ended up losing about Rs. 60 on it out of the total premium of Rs. 160, as we covered the calls today at Rs. 102. The puts remain in place and don’t have much value, but we’ll leave it in there.

We also bought extra 6500 puts at about Rs. 60, which have only Rs. 10 left in them. We’ll roll them over to April as our indicators still expect a downmove.

This has been a rough month on Index options. We made some money on an earlier straddle (6300), we lost about half that on the 6500 straddle, and we are losing that much on open put options. However, stocks have done well in the portfolio and will readjust.

Note: We’re not actively speaking of positions that are very short term because of the time it takes to put in the information into a consumable format. We will evolve a simpler, shorter table format for those positions where we don’t need to explain all that much.

Conclusion

Options are very useful in setting up positions that benefit from volatility that certain events like elections bring about. To not over pay or to reduce risk, we can set up non-directional positions (that is, positions that benefit from a move in either direction) through Condors and Butterflies.

We can still continue to trade directionally through Option Spreads or naked options. We could use straddles and strangles as well. However, these are not looking to be very useful at this time.

The one negative about Condors and Butterflies is that they involve losing more money when you lose, than the money you make when you win. But they are taken only when you believe strongly that the probability of them moving a lot is very high. Essentially you bet on 10%+ moves, and elections certainly seems like a viable candidate for such a move.

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

[/level-capmind-pro]