This is an archive for Capital Mind Premium subscribers. To know more, click here.

It’s been a few quiet days at Capital Mind as the anti-histamines have turned our brains into jelly. The situation has now improved considerably, which lets us look at the pieces of data that came in over the week. Today’s piece is about how the RBI has borrowed from our tomorrow to make our today look better.

Summary

- RBI’s Bulletin shows a $10 billion net ‘purchase’ of the US Dollar.

- In reality it is $8 billion of net ‘sales’, thanks to forward obligations.

- Look, we’re back to 2007 on the RBI forex reserves pieces, if you consider forward obligations.

- The impact, on liquidity and inflation.

[level-capmind-pro]

The last year was quite tough on the rupee. The RBI “rescued” it though an FCNR swap, inviting non residents to invest in dollar denominated assets for three years, which brought in dollars today against a repayment obligation after three years. Nearly $34 billion was brought in through this measure and the dollar went from Rs. 68 to Rs. 62 in a short span.

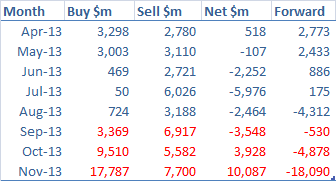

The real cost of this operation has now been revealed. The RBI’s $34 billion move brought in forex today, but also brought in a “forward” obligation three years into the future. These obligations are detailed in an RBI statement that comes in once a month in the RBI bulletin, with a two month lag. We now have data till November, when the FCNR swap ended. Look at the three months of the FCNR swap:

The RBI bought $17 billion in November, while selling $7 bn. The buying was obviously the FCNR swap – where banks got dollar funds from NRIs and sold them directly to the RBI, as part of a three year swap, when RBI would return the dollars after three years charging the Indian currency 3.5%,

The RBI selling could have been in two parts – either direct sales in the market, or sales to oil companies (who are the biggest purchasers of dollars at around $7 bn a month). However, in November, RBI Governor Rajan had mentioned that the oil companies were buying directly from the market, in an effort to calm down market fears. There, I had mentioned my surprise at the RBI holding an OMO (Open Market Operation) to buy rupee bonds and thus augment liquidity – this could have only come if the RBI had been selling lots of dollars in the market. Which is true, it turns out.

I believe the RBI has been selling dollars. If they sold $1.5 billion over the last few days, they would have taken Rs. 8000 to 9000 cr. out of the liquidity in the markets. To build that back, they will do an OMO – where they purchase bonds from banks and give them rupees.

It’s apparent the RBI sold a lot more – they sold over $7 billion in the month!

Why should we care?

The point is: the rupee did not stabilize because of the FCNR swap. It was the RBI taking those dollars and intervening directly in the market that caused the reversal. Effectively our regulator has been directly selling dollars to “calm down” fears.

This also means that the “fundamental” reason for the rupee to stabilize is not strong. The reason is simply dollar selling by the RBI. It’s not because of higher exports. It’s not because of strong foreign investor inflows, other than the FCNR swap which was a risk-free leveraged deal offered to rich NRIs who could arbitrage the interest rates within.

What’s the damage?

Obviously someone’s going to pay for this. It’s the “us” that will survive another three years – till 2016 November, to be exact.

If you look at the total forward exposure that the RBI currently has, it is a net forward “sale” of $32 billion, of which $18 billion came in November alone. So although they net bought $10 billion in the spot market, we see a much bigger sale in the “three year forward” market, when they will have to sell the dollars and make good their promise.

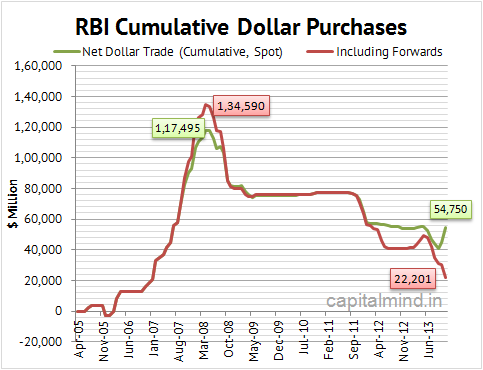

We’re back to 2007

The real damage is evident if you plot the total RBI purchases (minus sales, including forward exposure) since 2005.

While November looks juicy, it’s important to note that net of forwards, the RBI has taken cumulative buys back to the 2007 level!

While forex reserves have stabilized (they are announced every week, but the forwards are not) the net result, after considering forwards, is back to levels last seen in September 2007.

Isn’t that good?

RBI’s purchase of dollars is inflationary. To buy dollars, they print more rupees, and those rupees slosh around in the system and, in a decreasing savings rate situation, cause inflation as it’s more money chasing the same goods. This has caused, in my opinion, nearly all of the inflation that we are seeing in consumer prices. So a return of the RBI to the old times by selling dollars should be a good thing, no?

Not if the bulk of the “sales” are forward sales, intended to be complete at another time. The above graph shows we are actually printing more rupees today, but promising to sell even more dollars back in three years. The green line is going up, while the red line is sloping down!

I would have preferred dollar sales today. We inflated when foreigners invested. We should deflate and let the dollars go when things go the other way. It will also help curb inflation. In any case, the RBI has no business trading the rupee directly – it should not be allowed to, especially as a regulator of the forex market. Stability is bullshit; we are mature people that can easily live with short term volatility, which will settle down to find the next stable level by itself. We should, in my opinion, just dump our forex reserves and let the rupee go completely free.

This means two things:

- Inflationary pressure today. With the $10 billion of “net” purchases, banks have about Rs. 60,000 cr. more rupees than earlier. That extra money is currently sitting with banks and relieving some pressure on liquidity, where overnight borrowings from the RBI have reduced. Should credit growth resume, we are likely to see the advent of extreme inflation yet again.

- Liquidity pressure tomorrow: In three years, the RBI will have to pay back the $32 billion in forwards that they owe. They will have to dip into reserves, but more importantly, they will have to take rupees from banks in exchange. These rupees, which at Rs. 60 to the dollar will total around Rs. 200,000 crores, will go out of circulation. If the situation then is anywhere like now, this will cause massive damage to the rupee market (you can easily see short term rates

spike to high double digits). The RBI will end up doing something else that’s equally short term or silly to alleviate that pain – we will go from one bandage to another, transferring the eventual damage another few years down the line.

RBI’s options to redo another FCNR trick in 2016 will be limited. Already with the US taper, US 10 year rates are at 3%. If US bonds (three year duration) trade around the 5% mark which is more normal, after three years, the FCNR trick will simply not fly. It flew this time because borrowing rates for NRIs was 3% and they could place dollars with Indian banks at 5.5%, backed by the RBI. If US bonds trade at 5% there is no arbitrage as borrowing rates will be higher.

Impact

In the short term, the excess liquidity will help keep longer term bond rates under control, regardless of the rising fiscal deficit we are seeing nowadays. Couple that with a return to “risky” bonds in the west – bond prices of peripheral euro countries, the PIIGS, have been rising – and we might see foreign investor interest in Indian bonds rise too. This should naturally help the rupee.

However, in the longer term, this is an oncoming train wreck which we will do well to not ignore. It is important that we get our house in order – more exports, more foreign investors, lower inflation – fast, otherwise all we will get is the Great Crisis of 2016.

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

[/level-capmind-pro]